Lessons Learned from the Tax Court: What’s at Stake?

Astute readers of this publication may recognize that I frequently write on Cryptocurrency and also on Tax Court cases. It feels like Christmas to me to be able to write about a tax court case about crypto. This is only the Third Tax court case to even mention crypto, and the first to look at the underlying principles of taxation. (The other two were about including crypto assets in a CDP hearing and a frivolous tax protester argument). Today’s case, Paschall v. Commissioner, is about the taxation of staking income.

READ MORETAX COURT ROUNDUP – May 2026

April brings both anomalies and the same-old from Tax Court. Congressional enactments that misfire give opportunities to inventive practitioners, while self-represented petitioners continue to do the darndest things. All these are teaching moments that make "the small court" a continuing professional education course that never ends.

Read More

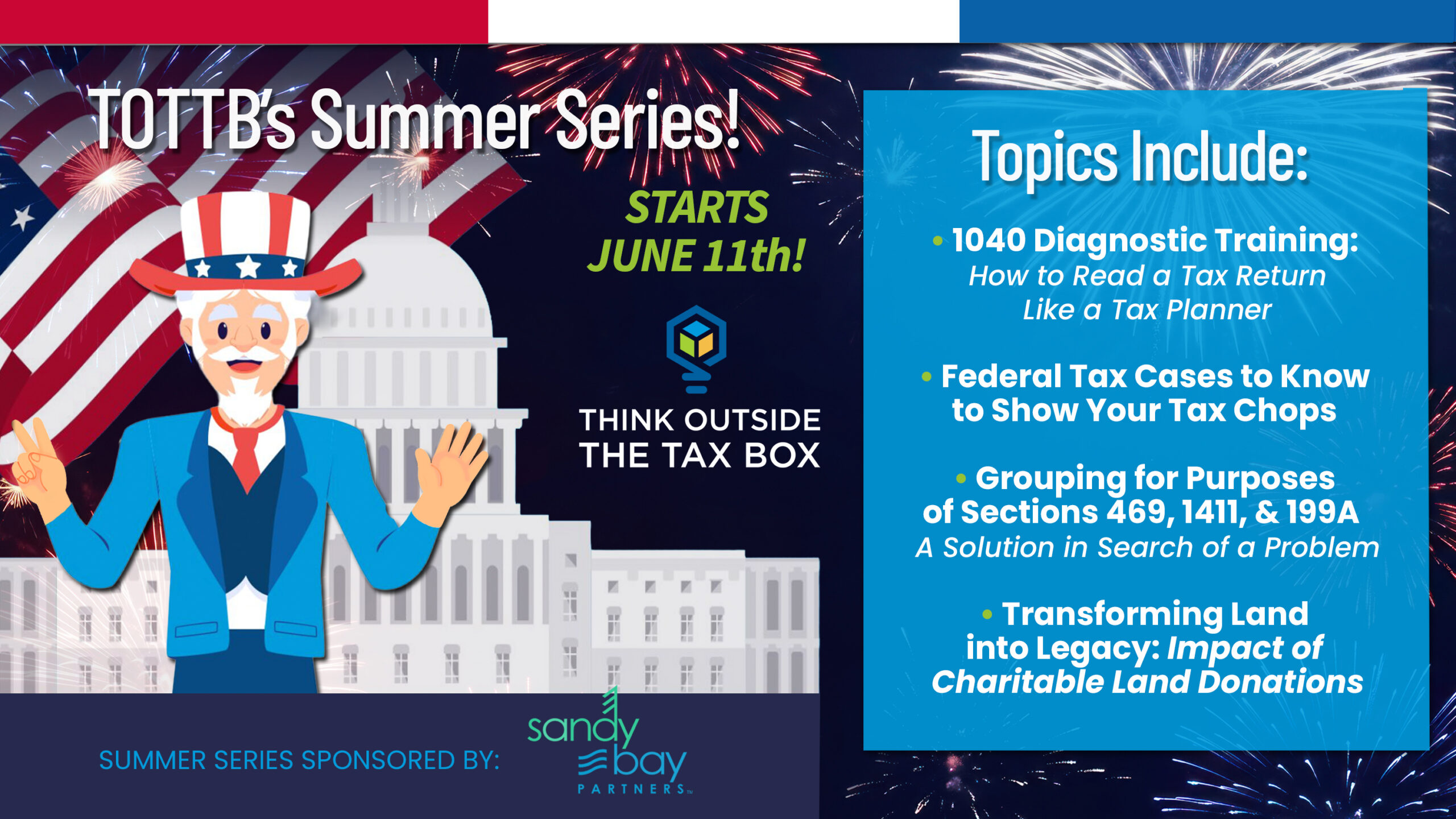

2026 Summer Education Series Event Calendar

Think Outside the Tax Box is thrilled to bring you the 2026 Summer Education Series, sponsored by Sandy Bay! The fifth installment of this beloved annual series, we will be bringing our loyal subscribers monthly webinars featuring some of the brightest minds in tax all summer long. Each webinar will feature our usual blend of high-quality education and entertainment and include continuing education credits for those who qualify. All of this is included in your regular subscription! Continue reading to see what we have in store...

Read More

Tax Loss Harvesting with Cryptocurrency

In the Fall of 2025, Bitcoin reached an all-time high of over $120,000. Since then, it fell over 40% to under $70,000 in the first quarter of 2026, before slightly recovering, currently resting around $75,000 as of this writing. With the steep drop in the price of Bitcoin and other cryptocurrencies, a common question from taxpayers is whether they can use the current losses to offset their other income. Large investors and professionals such as Grant Cardone and Shehan Chandrasekera (Head of Tax Strategy at Cointracker) have suggested that cryptocurrency can be sold and bought back immediately to claim the tax benefits. As with most things, the answer to this is not as simple as they portray, and many commentators, influencers, and sometimes professionals, miss the intricacies of cryptocurrency taxation.

Read More

The Kwong Tsunami: Why Form 843 Claims Could Soon Flood Your Practice

The buzz around the Kwong v. United States decision is quickly turning into something very real for practitioners: potentially a wave of Form 843 claims tied to COVID-era penalties and interest. With voices like Frank Agostino pushing for action, the message is clear: dig into client transcripts and don’t sit this one out, even though the outcome is still being litigated.

Read More

The Strategic Tax Analysis Process: Your Systematic Approach

Early in my career as a tax professional, I thought identifying strategic opportunities was primarily a function of technical knowledge. If I just knew enough tax law, I assumed the right strategies would naturally reveal themselves when reviewing a client's situation. This assumption led to a haphazard approach where I might spot a planning opportunity for one client but completely miss an identical opportunity for another simply because I wasn't methodically looking for it. This inconsistent approach changed when, leaning on my training as an instrument rated pilot, it occurred to me that I should be following a structured process that assures that I won’t miss any opportunities. That observation transformed my practice. I realized that identifying strategic opportunities isn't just about what you know—it's about how systematically you apply that knowledge. Even the most knowledgeable tax professional will miss opportunities without a structured methodology for uncovering them. In this article, I'll share the systematic strategic analysis process I've developed over three decades of tax practice. This methodology doesn't replace technical knowledge—it magnifies its impact by ensuring you consistently identify opportunities across diverse client situations.

Read More

The Brain Rust Effect: 100 Ways Accountants Are Fighting Cognitive Atrophy in the Age of AI

The accounting world is changing fast. Computers and AI now handle much of the boring, repetitive work that humans used to do by hand. This is great for saving time and catching mistakes, but it also introduces a new challenge: "mental rust" or “cognitive atrophy.” If we rely on computers for most of our thinking, our own problem‑solving skills can weaken. Recent studies suggest that heavy reliance on AI tools is associated with lower scores on some critical thinking tests. When we stop practicing how to solve problems ourselves, we may be less prepared when something unusual happens that the computer cannot handle. To stay sharp, accountants need to find practical ways to keep their brains working hard. Here are 100 simple ways to keep your mind strong in the age of AI.

Read More

Kwong v. United States: A Pandemic-Era Decision That Could Reshape Tax Deadlines, Penalties, and Refund Opportunities

The 2025 court decision, Kwong v. United States, is quietly gaining traction among tax professionals for exactly these reasons. Its implications could be far-reaching, potentially opening the door to refund claims, penalty abatements, and revived tax deadlines that many assumed were long closed. But there’s a catch: the opportunity to act may be time-sensitive, and the window to preserve claims could begin closing in just a few short weeks. Here’s what the court actually decided and why it matters now.

Read More

Untapped State Benefits for Veterans: Planning Opportunities for Advisors and Families

Two veteran clients with seemingly similar financial profiles can end up with very different outcomes, simply based on where they live and how informed they are. Much of that difference comes down to smaller, state-specific benefits that tend to sit just outside the typical planning checklist. But when layered alongside federal veteran benefits, they can reshape major decisions like where to buy a home or settle long-term. For advisors working with military families, recognizing how these state benefits show up in real life can go a long way in helping veteran clients feel seen, understood and better supported in the decisions ahead.

Read More

Lessons Learned from the Tax Court: What’s at Stake?

Astute readers of this publication may recognize that I frequently write on Cryptocurrency and also on Tax Court cases. It feels like Christmas to me to be able to write about a tax court case about crypto. This is only the Third Tax court case to even mention crypto, and the first to look at the underlying principles of taxation. (The other two were about including crypto assets in a CDP hearing and a frivolous tax protester argument). Today’s case, Paschall v. Commissioner, is about the taxation of staking income.

What’s New With Hobby Loss: Recent Developments in Section 183

Recent developments in the Section 183 (Hobby loss) area have not led me to change my basic conclusions. Taxpayers who have a sincere objective of ultimately making a profit should not hesitate to claim losses from the underlying activities. That is so even if you believe that profits are improbable. It is critical that they meet the standard of behaving in a businesslike manner. The other regulatory factors should not be ignored, but often there is not that much you can do about them. Reilly’s 18th Law of Tax Planning – Honest objective trumps realistic expectation.

The Art of Income Shifting: Powerful Planning Strategies That Stand Up to Scrutiny

Income shifting strategies address taxation at its most fundamental level by directing income to taxpayers in lower brackets or with offsetting deductions. Unlike many tax strategies that merely time recognition or enhance deductions, effective income shifting can permanently reduce the tax burden on a given dollar of income—often creating tax savings that compound year after year. In this article, we’ll explore systematic approaches to income shifting that create extraordinary value for clients while maintaining impeccable compliance.