A Court Just Bought Your Clients More Time on Clean Energy Tax Credits Here’s How to Use It

A federal district court just struck down an IRS rule that had been closing the door on a pretty compelling tax savings opportunity available to your clients today, the Section 48E Clean Electricity Investment Tax Credit. The ruling, handed down on June 6, 2026, reinstated a key pathway that allows investors to lock in credit eligibility for large-scale wind and solar projects a pathway the IRS had tried to eliminate just last year. The window is not wide open. July 4, 2026 is still the critical deadline, and the government will almost certainly appeal. But for advisors who act quickly, this ruling creates a genuine, time-sensitive planning opportunity. Here is what you need to understand, and what you should be doing right now.

READ MOREWorrisome Messages Subtly Delivered Via Recent Tax Developments

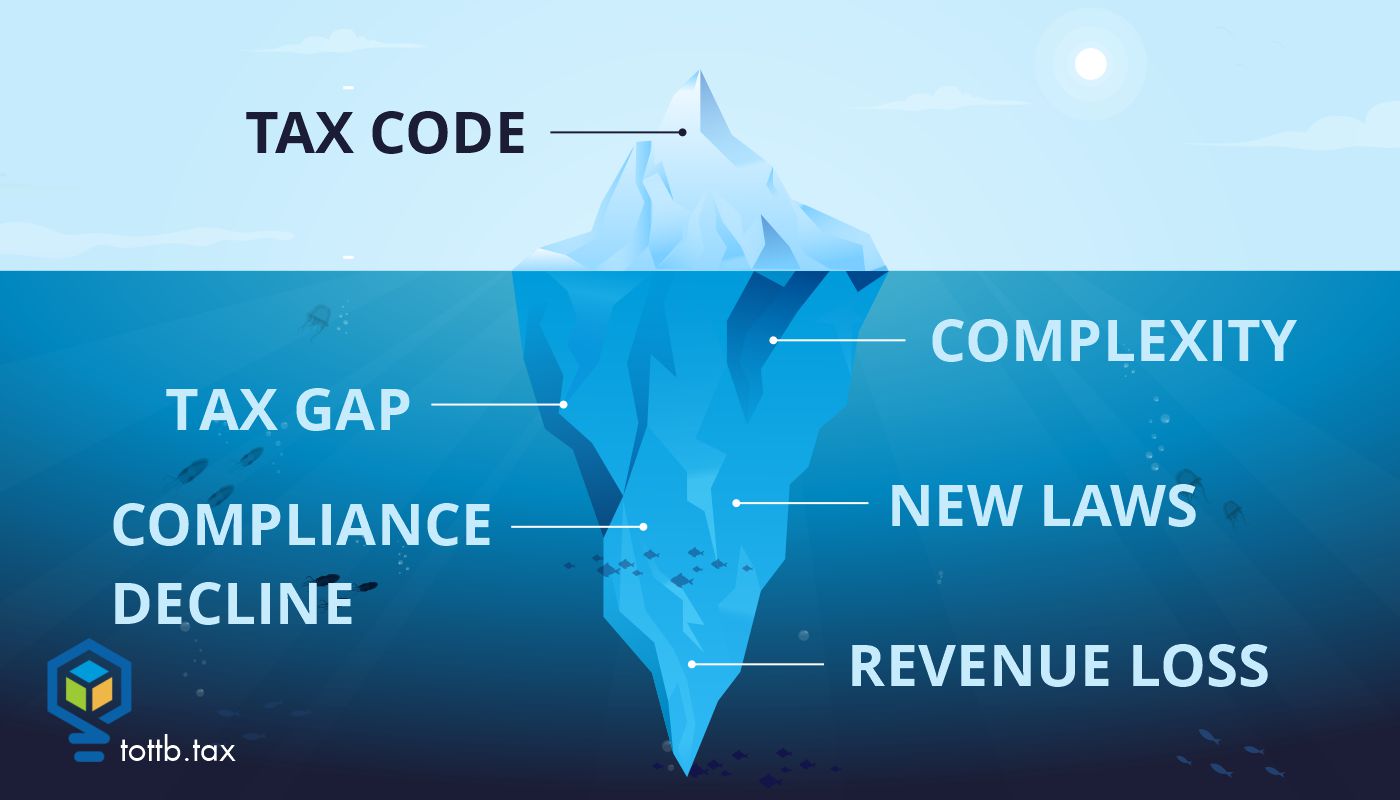

Tax professionals are inundated with tax developments from all branches of the government and from all levels of government on a daily basis. Our technical tax knowledge expands weekly. Given the immensity of tax law changes in P.L. 119-21 (July 4, 2025), informally named the One Big Beautiful Bill Act (OBBBA), and the guidance we’ll continue to get over the next few years along with non-OBBBA updates, we might run out of time and bandwidth to step back and ask what additional relevance this guidance, as well as various reports issued by the government every day, mean for the well-being of our tax system. This article unpacks select tax law changes and government documents to offer four subtle messages within them. Generally, the messages don’t bode well for an effective tax and revenue system. The article ends with some suggestions on what can help improve our tax system.

Read More

Sirius Solutions and the S Corp or Partnership Choice

The Fifth Circuit Court of Appeals opinion in Sirius Solutions L.L.L.P. v. Commissioner may change our views of entity choice. If the decision holds up, partnerships will be able to effectively make the portion of limited partner income subject to self-employment tax whatever they want, including zero. This contrasts with the IRS position upheld by the Tax Court in Soroban Capital that treated all of the income of limited partners who were active in the business as self-employment income.

Read More

Niche Down to Scale Up: How Specialization Drives Visibility and Profitability

For many accountants, narrowing our focus can feel risky. We are trained to serve anyone who needs help and provide stability in any financial situation. Choosing a niche often raises concerns: Will we turn away good clients? Will we limit opportunities or reduce business stability? These are common doubts many of us have faced in our careers.

Read More

TAX COURT ROUNDUP – May 2026

April brings both anomalies and the same-old from Tax Court. Congressional enactments that misfire give opportunities to inventive practitioners, while self-represented petitioners continue to do the darndest things. All these are teaching moments that make "the small court" a continuing professional education course that never ends.

Read More

2026 Summer Education Series Event Calendar

Think Outside the Tax Box is thrilled to bring you the 2026 Summer Education Series, sponsored by Sandy Bay! The fifth installment of this beloved annual series, we will be bringing our loyal subscribers monthly webinars featuring some of the brightest minds in tax all summer long. Each webinar will feature our usual blend of high-quality education and entertainment and include continuing education credits for those who qualify. All of this is included in your regular subscription! Continue reading to see what we have in store...

Read More

Tax Loss Harvesting with Cryptocurrency

In the Fall of 2025, Bitcoin reached an all-time high of over $120,000. Since then, it fell over 40% to under $70,000 in the first quarter of 2026, before slightly recovering, currently resting around $75,000 as of this writing. With the steep drop in the price of Bitcoin and other cryptocurrencies, a common question from taxpayers is whether they can use the current losses to offset their other income. Large investors and professionals such as Grant Cardone and Shehan Chandrasekera (Head of Tax Strategy at Cointracker) have suggested that cryptocurrency can be sold and bought back immediately to claim the tax benefits. As with most things, the answer to this is not as simple as they portray, and many commentators, influencers, and sometimes professionals, miss the intricacies of cryptocurrency taxation.

Read More

The Kwong Tsunami: Why Form 843 Claims Could Soon Flood Your Practice

The buzz around the Kwong v. United States decision is quickly turning into something very real for practitioners: potentially a wave of Form 843 claims tied to COVID-era penalties and interest. With voices like Frank Agostino pushing for action, the message is clear: dig into client transcripts and don’t sit this one out, even though the outcome is still being litigated.

Read More

The Strategic Tax Analysis Process: Your Systematic Approach

Early in my career as a tax professional, I thought identifying strategic opportunities was primarily a function of technical knowledge. If I just knew enough tax law, I assumed the right strategies would naturally reveal themselves when reviewing a client's situation. This assumption led to a haphazard approach where I might spot a planning opportunity for one client but completely miss an identical opportunity for another simply because I wasn't methodically looking for it. This inconsistent approach changed when, leaning on my training as an instrument rated pilot, it occurred to me that I should be following a structured process that assures that I won’t miss any opportunities. That observation transformed my practice. I realized that identifying strategic opportunities isn't just about what you know—it's about how systematically you apply that knowledge. Even the most knowledgeable tax professional will miss opportunities without a structured methodology for uncovering them. In this article, I'll share the systematic strategic analysis process I've developed over three decades of tax practice. This methodology doesn't replace technical knowledge—it magnifies its impact by ensuring you consistently identify opportunities across diverse client situations.

Read More

A Court Just Bought Your Clients More Time on Clean Energy Tax Credits Here’s How to Use It

A federal district court just struck down an IRS rule that had been closing the door on a pretty compelling tax savings opportunity available to your clients today, the Section 48E Clean Electricity Investment Tax Credit. The ruling, handed down on June 6, 2026, reinstated a key pathway that allows investors to lock in credit eligibility for large-scale wind and solar projects a pathway the IRS had tried to eliminate just last year. The window is not wide open. July 4, 2026 is still the critical deadline, and the government will almost certainly appeal. But for advisors who act quickly, this ruling creates a genuine, time-sensitive planning opportunity. Here is what you need to understand, and what you should be doing right now.

Your Summer Tax Practice Playbook: Three Moves to Make Before Labor Day

Tax Day is finally in the rearview mirror, and if you’re like many practitioners—with the phones quieter, the inbox manageable, and the September extension wave feeling comfortably far away—the temptation right now is to coast. Resist that temptation. Summer is the only stretch of the calendar when both you and your best clients have the bandwidth to think strategically; furthermore, this summer, there is a deadline-driven opportunity. In this article, I’ll walk through three moves every practitioner should be making between now and Labor Day. The first move has a hard statutory deadline of July 10, 2026. The second move is about turning your highest-value client conversations into billable advisory engagements. And third is about tending to the practice itself because a tax practice, like a garden, doesn’t survive without care.

What Every Client Should Know About Partnership Distributions

Perhaps the most misunderstood aspect of partnership taxation relates to distributions. When a partnership distributes cash or property to its partners, the tax consequences can range from completely tax-free to significantly taxable, depending on how the distribution is structured and the partners’ tax basis in their partnership interests. In this article, we’ll explore the rules governing partnership distributions and how they impact partners’ tax situations. More importantly, we’ll look at strategies to structure distributions in the most tax-efficient manner possible – because the goal is not just to understand the rules but to use them advantageously.