Lessons Learned from the Tax Court: What’s at Stake?

Astute readers of this publication may recognize that I frequently write on Cryptocurrency and also on Tax Court cases. It feels like Christmas to me to be able to write about a tax court case about crypto. This is only the Third Tax court case to even mention crypto, and the first to look at the underlying principles of taxation. (The other two were about including crypto assets in a CDP hearing and a frivolous tax protester argument). Today’s case, Paschall v. Commissioner, is about the taxation of staking income.

READ MOREPotential Pitfalls of Digital Assets and the “Kiddie Tax”

Those of us who are parents of Gen Z children know it’s “no cap ” that we have no clue what our children get up to on the internet. My son, for example, makes a lot of YouTube videos of our cat for some reason. Thankfully, he hasn’t monetized his videos (yet!), so they don’t carry any tax consequences. However, many taxpayers are finding out that their dependents have spent their time in the metaverse, defi gaming, or nfts, and as a result have engaged in dozens to thousands of taxable transactions without even being aware it. Those transactions may also trigger the “Tax on a Child's Investment and Other Unearned Income,” also known as the “Kiddie Tax.” Read on to learn more...

Read More

TAX COURT ROUND-UP – January 2023

I'm new here, but I know enough not to try to do what everyone else does. I won't try to cover the wider tax picture. I cover United States Tax Court on my blog, so here's a brief round-up on what went on in Tax Court during the last month that I think is of interest to the tax planner and practitioner...

Read More

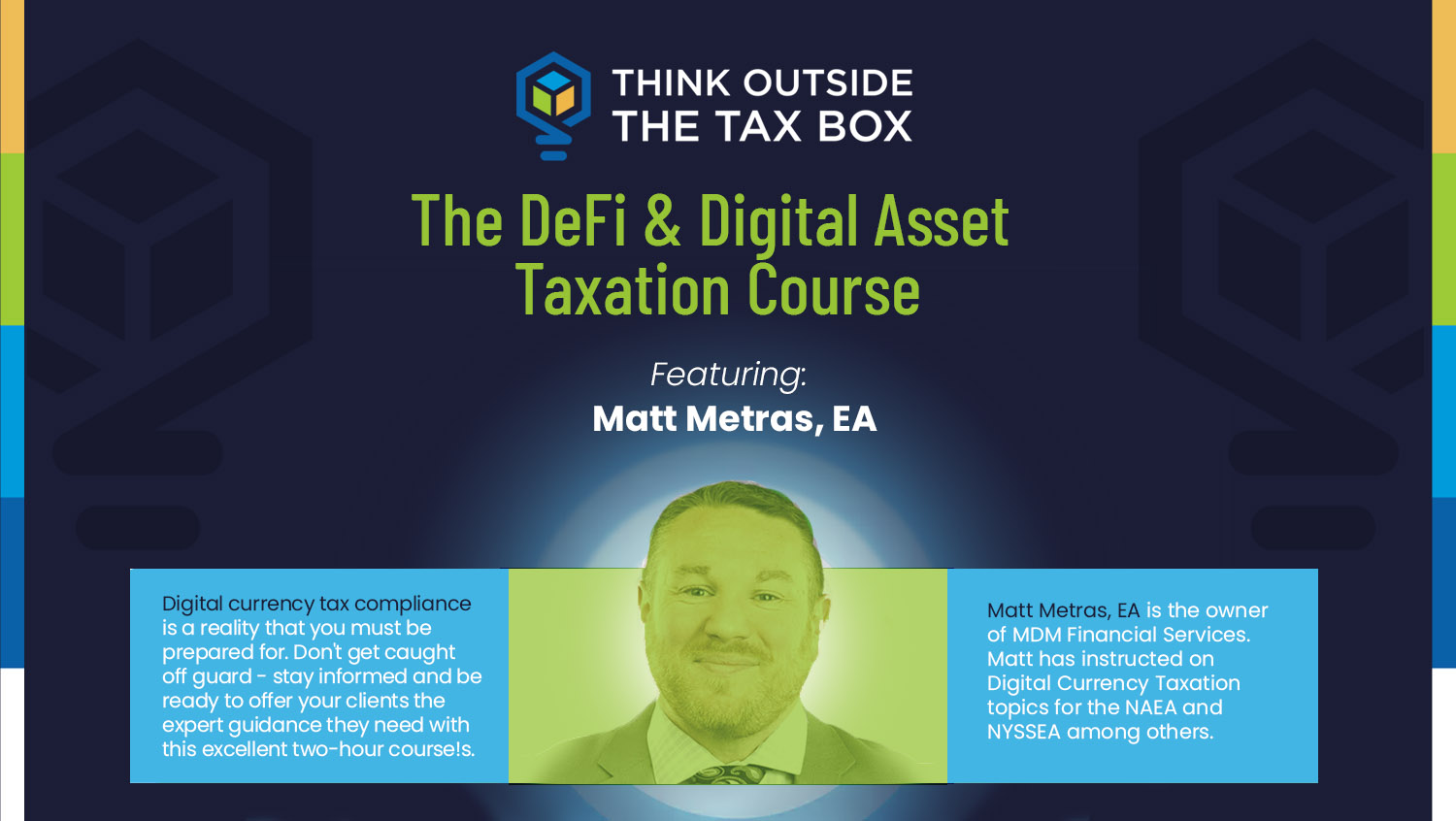

Live Webinar Event: The DeFi & Digital Asset Taxation Course

Join nationally recognized speaker and educator Matt Metras, EA, as he guides you through the ins and outs of mining, staking, forks, airdrops, DeFi swaps, yield farming, liquidity pools, NFTs, and more. With little guidance in these areas, you'll learn how to apply existing code sections to cryptocurrency situations, with a focus on finding tax-saving opportunities. We'll also cover how to extract transactions from the blockchain and introduce you to a number of helpful tools. This two-hour course is packed with valuable information, but it’s more than just information - we're also offering continuing education credits to qualifying attendees, courtesy of the American Institute of Certified Tax Planners.

Read More

Year End Tax Saving Tips for the Digital Currency Investor

As a financial expert, I know that 2022 has been a roller coaster year for investors. With only days left in the year, the Dow is down and the S&P 500 is down . On the high-risk crypto side, Bitcoin has fallen 64 percent and former Top 10 coin Solana has fallen more than 92 percent thanks to Sam Bankman-Fried and FTX. While the markets may be down, taxpayers can still come out ahead through careful tax planning. By taking the time to assess your financial situation and make strategic decisions, you can minimize their tax burden and potentially save money. It's important to consult with a tax planning professional to ensure that you’re taking advantage of all available tax savings opportunities. Here are a few of the things to do before the clock strikes midnight on New Year’s Eve.

Read More

Inflation Reduction Act – Energy Credits for Your Home

The Inflation Reduction Act has brought back and revised credits we have seen before. One of these credits had a $500 lifetime value but now can be $1,200 for each eligible tax year. That is a potential $11,500 increase in savings for your clients. They do not have to build a new house to take advantage of these savings. Taxpayers can receive this credit for improvements made to their home. The tax savings do not stop there. If your client buys an electric vehicle, they are going to need somewhere to charge it, right? Well, the Inflation Reduction Act has considered that, too. Homeowners can save an extra $1,000 on their taxes by installing the charging equipment at home. Let's explore how you can help your non-business clients capitalize on these types of tax savings on these improved energy credits. We will look at both credits now.

Read More

Making Smarter Retirement Account Distributions by Asking When, Why, and Where

As a proactive client, you often ask your tax professional about the tax effects of taking distributions from your retirement accounts. Unfortunately, it seems that proactive clients are in the minority. More often, your tax professional only learns about your retirement account distribution when the Form 1099-R arrives with your other tax documents. Proactive tax planners can improve their tax savings strategies by asking the when, where, and why that can help reduce negative tax consequences and can make you look like a problem-solving rock star to your clients. Whether you are looking for proactive ideas to implement on your own, or you want to be a problem-solving rock star with your tax planning clients, keep reading to learn how to make smart retirement account distributions.

Read More

Don’t Forget the Cohan Rule but Try Not to Need It

We are creeping up to the centennial of the Cohan rule. Learned Hand’s opinion for the Second Circuit in Cohan v. Commissioner came out on March 3, 1930 . I love this rule so much that I've made it the Prime Directive in my own book, Reilly’s Laws of Tax Planning: “If you don’t have documentation, at least have a plausible story.” However, subsequent legislation, changes in societal expectations, and the passage of time have eroded the usefulness of the Cohan rule for taxpayers. In recent years, there have been more instances of courts refusing to apply it than allowing its use. That’s why in Reilly’s Sixteenth Law of Tax Planning, I advise people to “being right without substantiation can be as bad as being wrong.”

Read More

Using S Corporations to Minimize FICA And Medicare Tax

When United States Tax Court Judge Paris issued the opinion in the case of Ryan Fleischer in 2016 , it caused quite a stir in the tax blogosphere. And from what I have been able to gather off the record it remains of interest. The Fleischer decision makes it very difficult, if not impossible for some financial professionals to use S corporations to mitigate self-employment tax. Rather than attack on reasonable salary, the IRS took an assignment of income approach, which succeeded throwing planners for financial professionals like Fleischer into a bit of an uproar...

Read More

Lessons Learned from the Tax Court: What’s at Stake?

Astute readers of this publication may recognize that I frequently write on Cryptocurrency and also on Tax Court cases. It feels like Christmas to me to be able to write about a tax court case about crypto. This is only the Third Tax court case to even mention crypto, and the first to look at the underlying principles of taxation. (The other two were about including crypto assets in a CDP hearing and a frivolous tax protester argument). Today’s case, Paschall v. Commissioner, is about the taxation of staking income.

What’s New With Hobby Loss: Recent Developments in Section 183

Recent developments in the Section 183 (Hobby loss) area have not led me to change my basic conclusions. Taxpayers who have a sincere objective of ultimately making a profit should not hesitate to claim losses from the underlying activities. That is so even if you believe that profits are improbable. It is critical that they meet the standard of behaving in a businesslike manner. The other regulatory factors should not be ignored, but often there is not that much you can do about them. Reilly’s 18th Law of Tax Planning – Honest objective trumps realistic expectation.

The Art of Income Shifting: Powerful Planning Strategies That Stand Up to Scrutiny

Income shifting strategies address taxation at its most fundamental level by directing income to taxpayers in lower brackets or with offsetting deductions. Unlike many tax strategies that merely time recognition or enhance deductions, effective income shifting can permanently reduce the tax burden on a given dollar of income—often creating tax savings that compound year after year. In this article, we’ll explore systematic approaches to income shifting that create extraordinary value for clients while maintaining impeccable compliance.