What Happens If You Can’t Use All Your Clean Energy Tax Credits This Year?

Clean energy tax credits have a lot going for them. Clients buy them at a discount, apply them dollar-for-dollar against federal tax liability, and walk away paying less to the IRS. That alone makes them worth a serious look. But here's what often gets overlooked and what makes these investments genuinely remarkable compared to almost anything else in your tax planning toolkit: the flexibility built into how and when the credits can be used. Can't absorb the full credit this year? Carry it back up to three years and trigger refunds on taxes your client already paid. Think about that for a second. There are very few places in the tax code where you can go back in time and rewrite last year's tax bill. This is one of them. Still have excess after the carryback? Carry it forward for up to 22 years. That's not a typo. Two decades of runway to put those credits to work as your client's passive income grows. And if circumstances change and the credits simply aren't needed? An emerging secondary market means there may even be an option to sell them. No other common tax planning strategy offers this combination a guaranteed discount on purchase, dollar-for-dollar offset of tax liability, the ability to look backward and forward, and a potential exit if plans change. Understanding how each of these features works is what separates a good credit investment from a great one.

READ MOREIRS Again Postpones Tax Reporting of $600 Payments

The federal government is there to reduce taxpayer confusion. That, at least, was one point of the reasoning for the recent IRS decision to again postpone a $600 tax-reporting threshold for people paid via third-party settlement networks. Those who made that amount on the likes of eBay and other online sales sites and who received payment via such platforms as PayPal and Venmo will not have that money reported to the IRS for another year. Does this really let taxpayers off the hook? What strategies should you adapt for when the IRS does mandate this reporting?

Read More

Mastering Email Marketing for Accountants: Strategies for Effective Client Communication

I knew little about email marketing when I started my entrepreneurial journey in 2018. I used emails to communicate regularly with team members, vendors, board members, etc. Little did I know that having an email list of prospects and effective campaigns are a way to grow revenues. We are in a time when digital communication, specifically email marketing, has been and continues to be one of the most potent tools for business owners, especially accountants, seeking to enhance client relationships and drive business growth. Many perceive that our accounting industry is traditional; however, we’ve finally included marketing in our world and established new avenues for engagement. Here, I will shed light on the crucial role of email marketing in the accounting sector and provide actionable strategies for effective client communication.

Read More

Staying Afloat in Tax Seas: Understanding the IRS’s Moratorium on ERC

Question: Should I even bother assisting my clients with filing new ERC claims? Answer: In light of the IRS's recent moratorium on processing new Employee Retention Credit (ERC) claims and the introduction of a withdrawal option for certain employers, it's understandable that you might be wondering whether to assist your clients with filing new claims. The answer, like a well-prepared tax return, is nuanced and deserves a detailed examination.

Read More

Time for Year-End Tax Planning

This year is far from over for tax planning – for some moves, you have even longer – but now’s the time to start looking and acting on your tax tactics given your circumstances and the 2023 you’ve had so far. What you do or don’t do now could save or cost you next April.

Read More

An Alphabet Soup of Confusion: LLCs, BOI, and UPL

By now I hope that all tax professionals have heard of the FinCEN requirement for certain entities to report beneficial ownership information starting in 2024. The requirement is causing confusion because tax and accounting professionals feel that this could be an opportunity to either add value to an existing engagement, could be a new revenue stream, or could be a huge potential for liability. What follows is a brief review of the law and the requirements, an analysis of the main issues, and some recommendations for practitioners wondering how to help their clients while limiting their professional liability.

Read More

TAX COURT ROUNDUP – NOVEMBER 2023

A very mixed bag this month: IRS shifting ground on the eve of trial, plenty of discovery, loyalty programs, the end of the road for meaningful Section 6751(b) supervisory approval, and arrival of a new Special Trial Judge. And, as always, a lot of questions.

Read More

Electronic Commerce Creates Confusing Sales Tax Obligations

Any company engaged in e-commerce, i.e., selling online, knows that the ability to reach buyers and customers remotely can juice the bottom line. State and local tax jurisdictions around the country know that, too, especially the bottom line of their sales tax coffers. Now every state with a statewide sales tax has a threshold past which remote sellers must collect and remit state sales tax. Failure to do so can incur big penalties, or worse, and there’s a lot to know based on where and what you sell online.

Read More

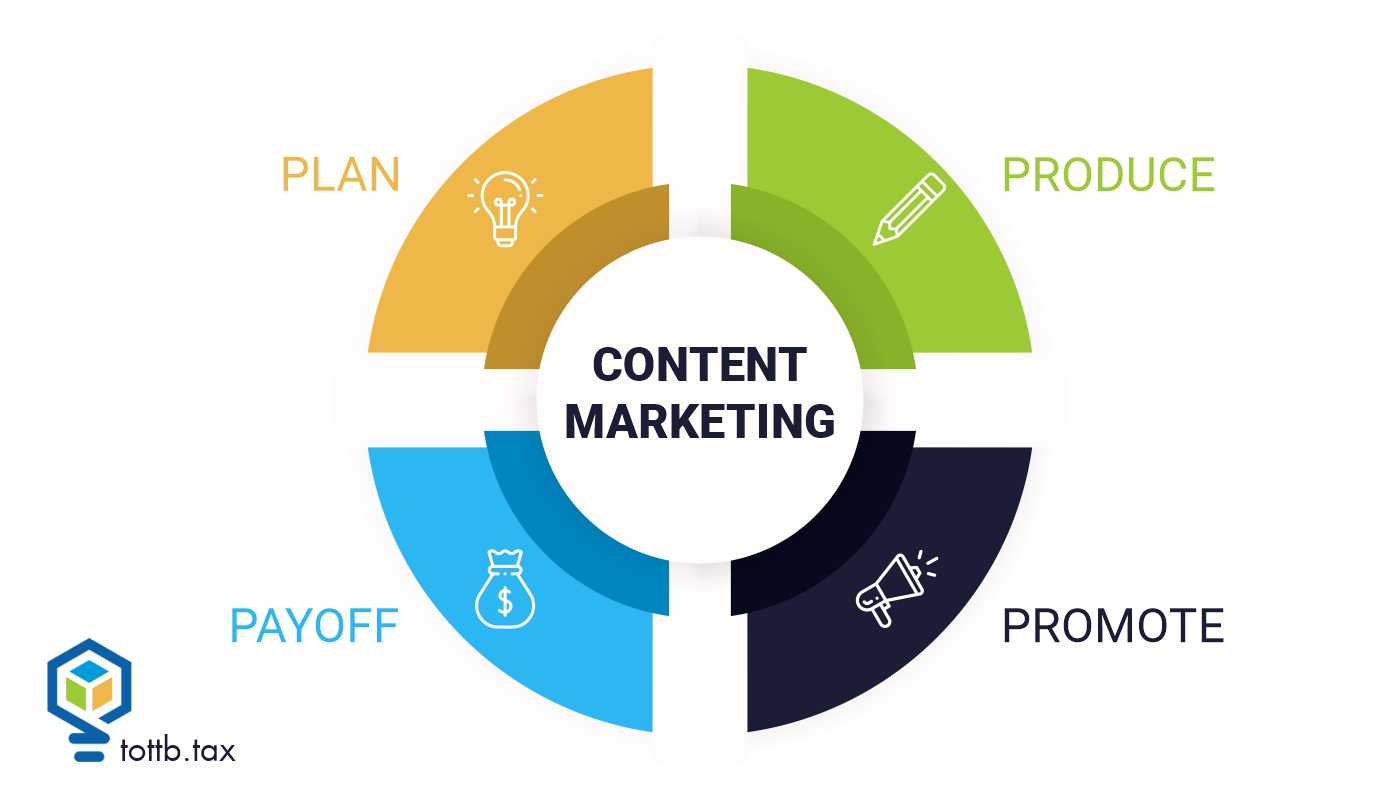

Content Marketing for Accountants: Creating Valuable and Engaging Content

If you read my article Building a Strong Personal Brand as an Accountant: Strategies for Success you’d have learned about how I started my entrepreneurial journey in 2018, knowing absolutely nothing about marketing. I was one of those CFOs who would need to understand why a company has to spend more money on marketing; however, I did understand that having a robust online presence was necessary for a new digital age. Little did I know that marketing is senior to any other activity in a business.

Read More

What Happens If You Can’t Use All Your Clean Energy Tax Credits This Year?

Clean energy tax credits have a lot going for them. Clients buy them at a discount, apply them dollar-for-dollar against federal tax liability, and walk away paying less to the IRS. That alone makes them worth a serious look. But here’s what often gets overlooked and what makes these investments genuinely remarkable compared to almost anything else in your tax planning toolkit: the flexibility built into how and when the credits can be used. Can’t absorb the full credit this year? Carry it back up to three years and trigger refunds on taxes your client already paid. Think about that for a second. There are very few places in the tax code where you can go back in time and rewrite last year’s tax bill. This is one of them. Still have excess after the carryback? Carry it forward for up to 22 years. That’s not a typo. Two decades of runway to put those credits to work as your client’s passive income grows. And if circumstances change and the credits simply aren’t needed? An emerging secondary market means there may even be an option to sell them. No other common tax planning strategy offers this combination a guaranteed discount on purchase, dollar-for-dollar offset of tax liability, the ability to look backward and forward, and a potential exit if plans change. Understanding how each of these features works is what separates a good credit investment from a great one.

Perspectives on IRS Scrutiny of Captive Insurance Elections

The Internal Revenue Service has made no secret of its increased scrutiny of captive insurance arrangements, particularly those involving the small insurance company election. For taxpayers and their advisors, this has created understandable concern and, in some cases, hesitation about whether captive insurance remains a viable risk management and tax planning tool. Yet heightened scrutiny does not mean prohibition. The Internal Revenue Code continues to recognize captive insurance, Congress has refined it, and courts evaluate it based on well-established insurance principles. The real issue is not whether captives are allowed, but whether a specific taxpayer has a legitimate business need for insurance, has structured the arrangement properly, and has implemented it in a manner consistent with both tax law and insurance fundamentals. Understanding where scrutiny arises, how elections function, and what separates compliant captives from problematic ones is critical for CPAs advising closely held businesses today.

Strict Substantiation: Why Being Right Without Proof Can Cost You Your Charitable Deduction

Reilly’s Sixteenth Law of Tax Planning – Being right without substantiation can be as bad as being wrong – is particularly apt when it comes to charitable contributions. The case law makes it clear that there is not much wiggle room in rules relating to substantiation and reporting of charitable contributions. We’ll dig into the rules here.