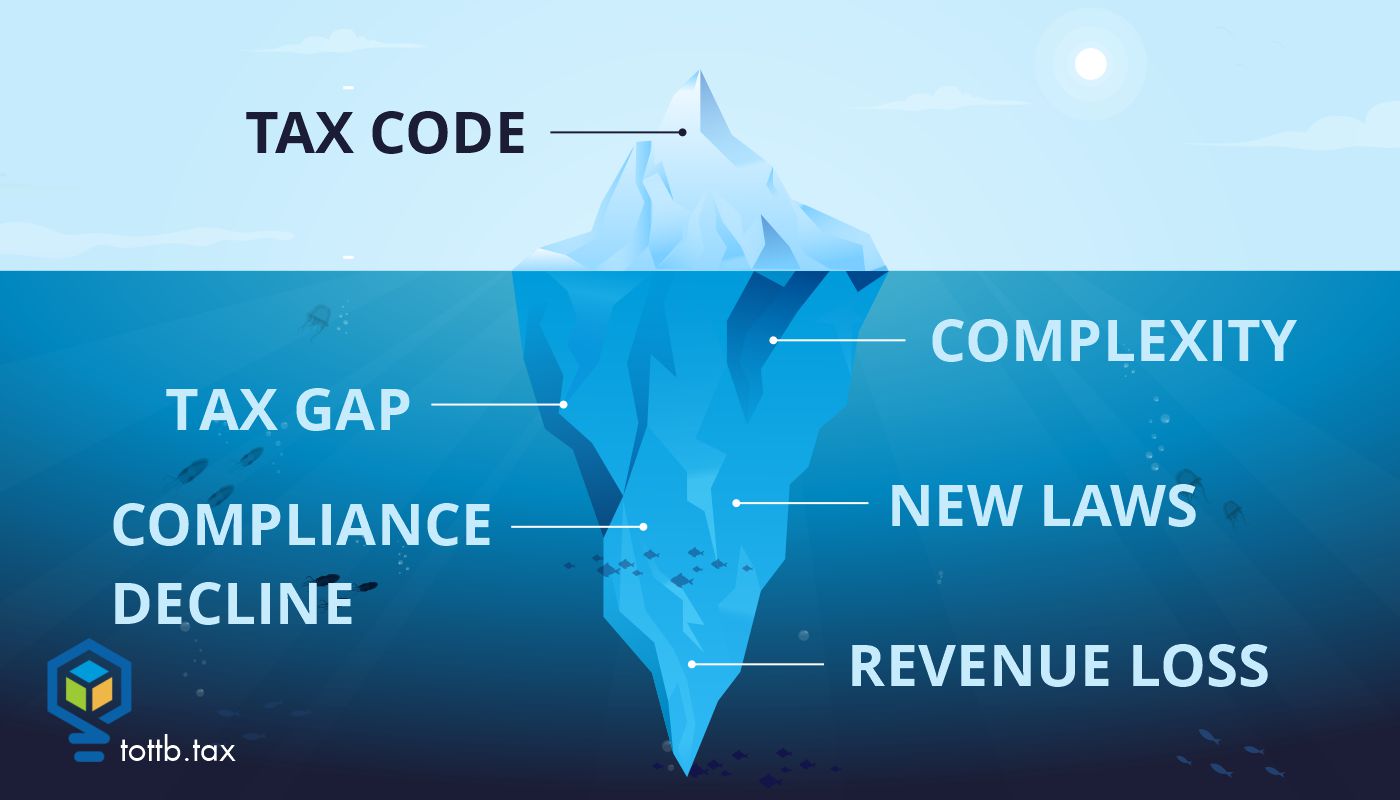

Worrisome Messages Subtly Delivered Via Recent Tax Developments

Tax professionals are inundated with tax developments from all branches of the government and from all levels of government on a daily basis. Our technical tax knowledge expands weekly. Given the immensity of tax law changes in P.L. 119-21 (July 4, 2025), informally named the One Big Beautiful Bill Act (OBBBA), and the guidance we’ll continue to get over the next few years along with non-OBBBA updates, we might run out of time and bandwidth to step back and ask what additional relevance this guidance, as well as various reports issued by the government every day, mean for the well-being of our tax system. This article unpacks select tax law changes and government documents to offer four subtle messages within them. Generally, the messages don’t bode well for an effective tax and revenue system. The article ends with some suggestions on what can help improve our tax system.

Sirius Solutions and the S Corp or Partnership Choice

The Fifth Circuit Court of Appeals opinion in Sirius Solutions L.L.L.P. v. Commissioner may change our views of entity choice. If the decision holds up, partnerships will be able to effectively make the portion of limited partner income subject to self-employment tax whatever they want, including zero. This contrasts with the IRS position upheld by the Tax Court in Soroban Capital that treated all of the income of limited partners who were active in the business as self-employment income.

Niche Down to Scale Up: How Specialization Drives Visibility and Profitability

For many accountants, narrowing our focus can feel risky. We are trained to serve anyone who needs help and provide stability in any financial situation. Choosing a niche often raises concerns: Will we turn away good clients? Will we limit opportunities or reduce business stability? These are common doubts many of us have faced in our careers.