What Happens If You Can’t Use All Your Clean Energy Tax Credits This Year?

Clean energy tax credits have a lot going for them. Clients buy them at a discount, apply them dollar-for-dollar against federal tax liability, and walk away paying less to the IRS. That alone makes them worth a serious look. But here's what often gets overlooked and what makes these investments genuinely remarkable compared to almost anything else in your tax planning toolkit: the flexibility built into how and when the credits can be used. Can't absorb the full credit this year? Carry it back up to three years and trigger refunds on taxes your client already paid. Think about that for a second. There are very few places in the tax code where you can go back in time and rewrite last year's tax bill. This is one of them. Still have excess after the carryback? Carry it forward for up to 22 years. That's not a typo. Two decades of runway to put those credits to work as your client's passive income grows. And if circumstances change and the credits simply aren't needed? An emerging secondary market means there may even be an option to sell them. No other common tax planning strategy offers this combination a guaranteed discount on purchase, dollar-for-dollar offset of tax liability, the ability to look backward and forward, and a potential exit if plans change. Understanding how each of these features works is what separates a good credit investment from a great one.

READ MOREAn Overview of the Risks and Possibilities of Related Party Exchanges

IRC § 1031 exchanges have the ability to confer substantial financial benefits to taxpayers. Although taxpayers may use § 1031 to place themselves in a superior economic position, taxpayers may not exploit this section in an abusive manner. Taxpayers can use exchanges to give themselves different types of benefits, but one of the primary benefits is the deferral of federal income tax. When conducted correctly, 1031 exchanges are regarded as a form of legitimate tax avoidance. One of the main issues involved with these transactions is determining the boundaries between abusive tax avoidance and non-abusive tax avoidance. In the context of “related party exchanges” – i.e. those transactions which involve subsection 1031(f) – this issue shows up in a relatively complex fashion, because the related party rules are not well understood by most practitioners. Furthermore, determining abusive tax avoidance with related party exchanges is difficult because of the scarcity of case law. Based on the case law which we have, and on the other authoritative references, we can put together a reasonable overview of the risks of related party exchanges. This overview should prove useful when providing expert counsel to taxpayers seeking to conduct this type of transaction. For direct exchanges, the 2-year ownership rule found in 1031(f)(1)(C) should be used as the dominant source of guidance. For “indirect exchanges,” taxpayers must be aware of the higher levels of risk involved, as there is a greater possibility of abusive tax avoidance. To read more click here!

Read More

Famous Bad Citizens and the Code That Caught Them – Al Capone

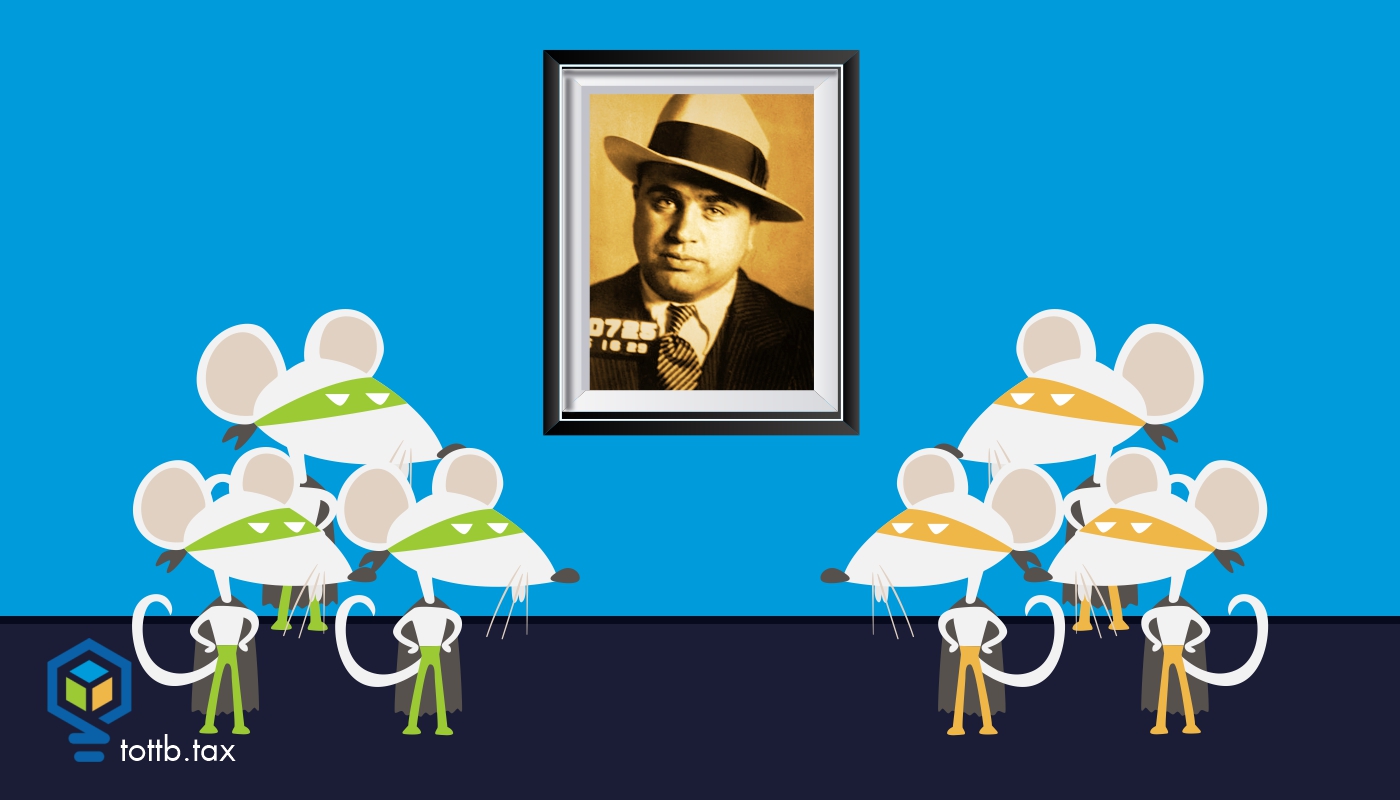

At its peak, Alphonse (Al) Capone’s criminal empire was worth approximately $1.3 billion when adjusted for inflation. On June 5, 1931, Capone was indicted on multiple counts of income tax evasion. At the time the maximum penalty for his offenses was 32 years in jail and $80,000 in fines (almost $1.6M in inflation adjusted dollars). The prosecution in Capone’s case “documented Capone's lavish spending, evidence of a colossal income. The government also submitted proof that Capone was aware of his obligation to pay federal income tax but failed to do so." Click here to keep reading about this fascinating case…

Read More

Vehicle and Mileage Issues – Real-World Best Practices and Maximizing Deductions in a Tax Plan

Every tax professional has at least one client that when asked about business mileage replies, “I don’t know; what did I have last year?” You may have read that last sentence and thought, “most of them.” Self-employed taxpayers generally know they must track their mileage, but it’s seldom done correctly, or at all. Vehicle deductions are an area frequently challenged by the IRS on examination as well as an area the taxpayer is unlikely to prevail without strong, contemporaneous documentation. That said, very few taxpayers keep perfect records, so what are the best practices for mileage deductions in the real world? Keep reading to find out!

Read More

Trump Indictment: An Accountant’s Perspective

IRC § 1031 exchanges have the ability to confer substantial financial benefits to taxpayers. Although taxpayers may use § 1031 to place themselves in a superior economic position, taxpayers may not exploit this section in an abusive manner. Taxpayers can use exchanges to give themselves different types of benefits, but one of the primary benefits is the deferral of federal income tax. When conducted correctly, 1031 exchanges are regarded as a form of legitimate tax avoidance. One of the main issues involved with these transactions is determining the boundaries between abusive tax avoidance and non-abusive tax avoidance. In the context of “related party exchanges” – i.e. those transactions which involve subsection 1031(f) – this issue shows up in a relatively complex fashion, because the related party rules are not well understood by most practitioners. Furthermore, determining abusive tax avoidance with related party exchanges is difficult because of the scarcity of case law. Based on the case law which we have, and on the other authoritative references, we can put together a reasonable overview of the risks of related party exchanges. This overview should prove useful when providing expert counsel to taxpayers seeking to conduct this type of transaction. For direct exchanges, the 2-year ownership rule found in 1031(f)(1)(C) should be used as the dominant source of guidance. For “indirect exchanges,” taxpayers must be aware of the higher levels of risk involved, as there is a greater possibility of abusive tax avoidance. To read more click here!

Read More

Divorce and Taxes

“Timalyn, Alyssa and I filed for divorce, and we will finalize everything before Thanksgiving. Does this change things for our taxes?” “No! Can we wait until January 1?” were my initial thoughts. But then I realized that if this news blindsided me, the seemingly happy couple was probably also scrambling for answers. They were looking to me to be calm during an upcoming storm. To give you some context, I had helped this family lower their back taxes by $16,000 and get a payment plan that worked well with their cash flow. Then, by implementing a few strategies they had just saved an extra $20,000 on their last tax return. We were planning on saving them even more money in upcoming years. Then, that is when it happened. Divorce. I never saw this happening, so I never prepared for it. But if it happened to me, it will happen to you. Clients divorce. Some of the things we are going over today may seem obvious to you. But remember what is obvious to us as tax experts is not obvious to our clients, especially if they are going through a life-changing event such as divorce. Here are four things you need to inform your client about when it comes to their divorce and taxes...

Read More

Facts, Circumstances, and Forever Stamps

The price of a forever stamp increased from $0.58 to $0.63 on January 1, 2023. A tax pro posted this fact as a public service announcement on Facebook. Of course, tax pros being tax pros, someone chimed in, “Do I have to recognize a capital gain upon disposition of my forever stamp?” And of course, someone (me) felt obliged to answer, “It depends.” A direct message followed this bit of tax drollery on Twitter that says, “In theory, if I’m holding stamps as an investment, they would be a capital asset.” And so it begins…

Read More

Crypto Charitable Deduction Compliance – Mission Impossible?

Reilly’s Fourth Law of Tax: “Execution isn’t everything, but it’s a lot” might be amended when it comes to charitable deduction of property, because there you have an area where execution is almost everything. It is also an area that dramatically illustrates the Seventh Law: “Read the instructions.” In January, we received guidance from the IRS on the reporting requirements for charitable contributions of crypto currency . If you have followed IRS guidance on crypto and know something about charitable donation reporting requirements, the result shouldn’t surprise you , but maybe it will. The most disturbing part of the story is that the IRS may be asking for something we can’t provide...

Read More

Tax Court Roundup – May 2023

As always, much has happened in the tax courts this past month; let's jump right in!

Read More

What Happens If You Can’t Use All Your Clean Energy Tax Credits This Year?

Clean energy tax credits have a lot going for them. Clients buy them at a discount, apply them dollar-for-dollar against federal tax liability, and walk away paying less to the IRS. That alone makes them worth a serious look. But here’s what often gets overlooked and what makes these investments genuinely remarkable compared to almost anything else in your tax planning toolkit: the flexibility built into how and when the credits can be used. Can’t absorb the full credit this year? Carry it back up to three years and trigger refunds on taxes your client already paid. Think about that for a second. There are very few places in the tax code where you can go back in time and rewrite last year’s tax bill. This is one of them. Still have excess after the carryback? Carry it forward for up to 22 years. That’s not a typo. Two decades of runway to put those credits to work as your client’s passive income grows. And if circumstances change and the credits simply aren’t needed? An emerging secondary market means there may even be an option to sell them. No other common tax planning strategy offers this combination a guaranteed discount on purchase, dollar-for-dollar offset of tax liability, the ability to look backward and forward, and a potential exit if plans change. Understanding how each of these features works is what separates a good credit investment from a great one.

Perspectives on IRS Scrutiny of Captive Insurance Elections

The Internal Revenue Service has made no secret of its increased scrutiny of captive insurance arrangements, particularly those involving the small insurance company election. For taxpayers and their advisors, this has created understandable concern and, in some cases, hesitation about whether captive insurance remains a viable risk management and tax planning tool. Yet heightened scrutiny does not mean prohibition. The Internal Revenue Code continues to recognize captive insurance, Congress has refined it, and courts evaluate it based on well-established insurance principles. The real issue is not whether captives are allowed, but whether a specific taxpayer has a legitimate business need for insurance, has structured the arrangement properly, and has implemented it in a manner consistent with both tax law and insurance fundamentals. Understanding where scrutiny arises, how elections function, and what separates compliant captives from problematic ones is critical for CPAs advising closely held businesses today.

Strict Substantiation: Why Being Right Without Proof Can Cost You Your Charitable Deduction

Reilly’s Sixteenth Law of Tax Planning – Being right without substantiation can be as bad as being wrong – is particularly apt when it comes to charitable contributions. The case law makes it clear that there is not much wiggle room in rules relating to substantiation and reporting of charitable contributions. We’ll dig into the rules here.