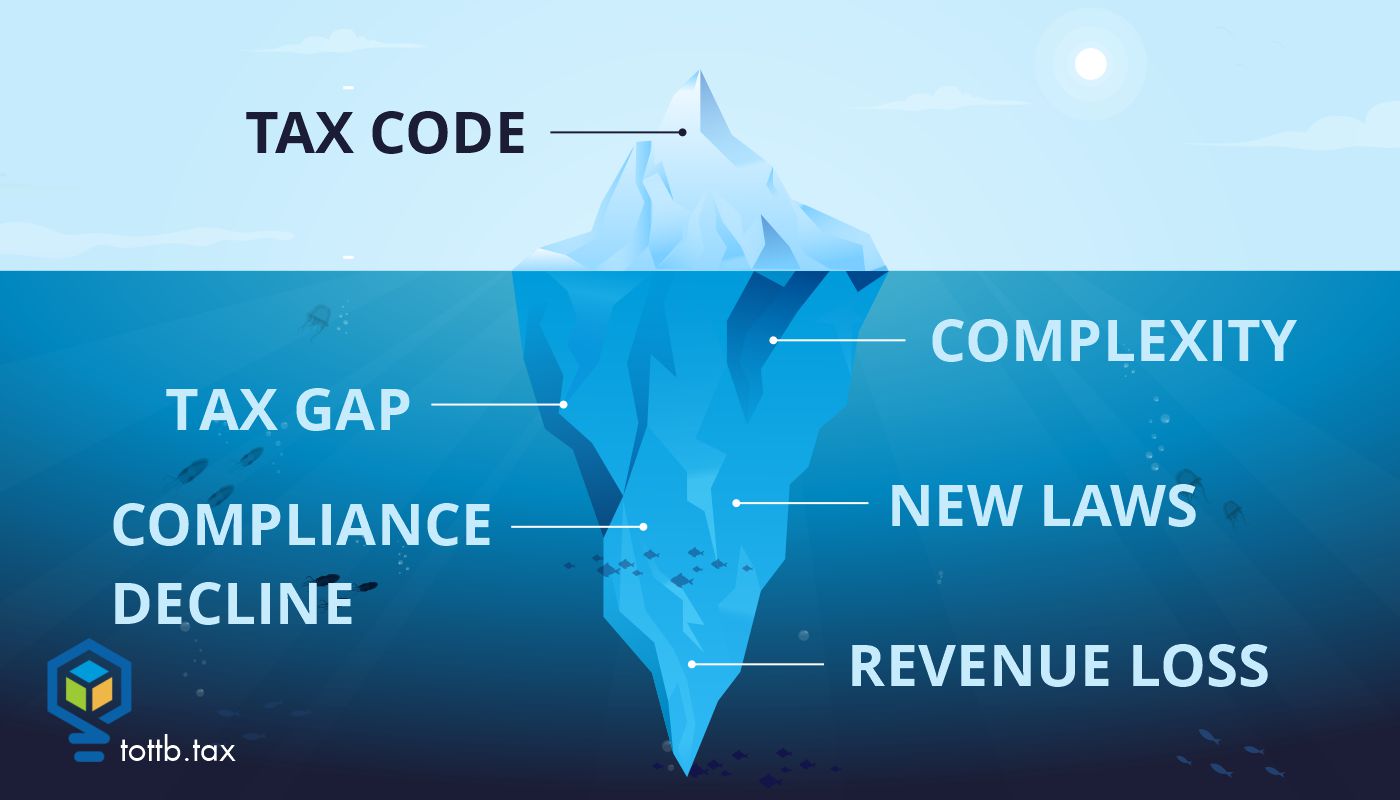

Worrisome Messages Subtly Delivered Via Recent Tax Developments

Tax professionals are inundated with tax developments from all branches of the government and from all levels of government on a daily basis. Our technical tax knowledge expands weekly. Given the immensity of tax law changes in P.L. 119-21 (July 4, 2025), informally named the One Big Beautiful Bill Act (OBBBA), and the guidance we’ll continue to get over the next few years along with non-OBBBA updates, we might run out of time and bandwidth to step back and ask what additional relevance this guidance, as well as various reports issued by the government every day, mean for the well-being of our tax system. This article unpacks select tax law changes and government documents to offer four subtle messages within them. Generally, the messages don’t bode well for an effective tax and revenue system. The article ends with some suggestions on what can help improve our tax system.

READ MORESophisticated Charity Plan Where Everything Goes Wrong

The story of Scott M. Hoensheid’s charitable planning gone awry as related by Judge Joseph W. Nega of the United States Tax Court is an interesting one. Click here to continue reading…

Read More

Are NFTs “Collectibles”? – The IRS Says Maybe

Beanie babies, Pokémon cards, POGs, and digital pictures of monkeys on the internet, one of these things is not like the others. All these are items that people may collect or at least have collected in the past. Maybe they were just collecting for fun, or perhaps they acquired in hopes of selling their items in the future for a profit. However, the IRS has highlighted only one of the items on this list as potentially being a collectible. A non-fungible token (NFT) “is a unique digital identifier that is recorded using distributed ledger technology and may be used to certify authenticity and ownership of an associated right or asset. Ownership of an NFT may provide the holder a right with respect to a digital file (such as a digital image).” NFTs run the gamut from bored apes (computer generated pictures of monkeys that sell for hundreds of thousands of dollars, not to be confused with board apes, which are monkey pictures on sandwich and surf boards and do not sell for hundreds of thousands of dollars) to Ruish Bronzelight (a DeFi Kingdoms online video game Warrior Wizard we met in “Tax Planning for DeFi Based Games”), and even event tickets (especially popular with crypto conferences). There is even at least one CPA who sells access to his tax practice via NFT. Click here to continue reading…

Read More

Tax Court Roundup June 2023

This month I've decided to change format. I'm grouping Tax Court thumbnails by category. Not every reader deals with every issue. But coverage is still useful even where only a few specialize. Click here to read the latest happenings!

Read More

An Overview of the Risks and Possibilities of Related Party Exchanges

IRC § 1031 exchanges have the ability to confer substantial financial benefits to taxpayers. Although taxpayers may use § 1031 to place themselves in a superior economic position, taxpayers may not exploit this section in an abusive manner. Taxpayers can use exchanges to give themselves different types of benefits, but one of the primary benefits is the deferral of federal income tax. When conducted correctly, 1031 exchanges are regarded as a form of legitimate tax avoidance. One of the main issues involved with these transactions is determining the boundaries between abusive tax avoidance and non-abusive tax avoidance. In the context of “related party exchanges” – i.e. those transactions which involve subsection 1031(f) – this issue shows up in a relatively complex fashion, because the related party rules are not well understood by most practitioners. Furthermore, determining abusive tax avoidance with related party exchanges is difficult because of the scarcity of case law. Based on the case law which we have, and on the other authoritative references, we can put together a reasonable overview of the risks of related party exchanges. This overview should prove useful when providing expert counsel to taxpayers seeking to conduct this type of transaction. For direct exchanges, the 2-year ownership rule found in 1031(f)(1)(C) should be used as the dominant source of guidance. For “indirect exchanges,” taxpayers must be aware of the higher levels of risk involved, as there is a greater possibility of abusive tax avoidance. To read more click here!

Read More

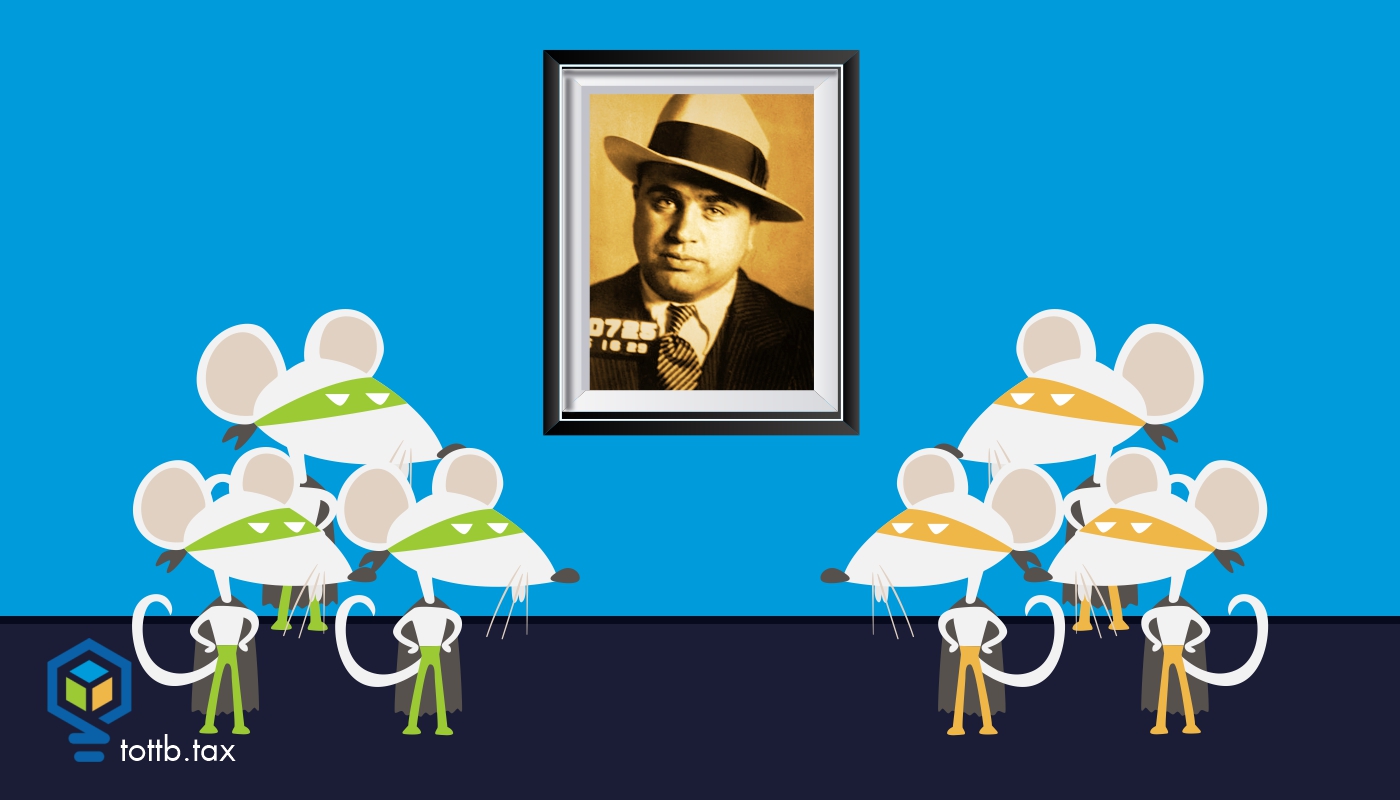

Famous Bad Citizens and the Code That Caught Them – Al Capone

At its peak, Alphonse (Al) Capone’s criminal empire was worth approximately $1.3 billion when adjusted for inflation. On June 5, 1931, Capone was indicted on multiple counts of income tax evasion. At the time the maximum penalty for his offenses was 32 years in jail and $80,000 in fines (almost $1.6M in inflation adjusted dollars). The prosecution in Capone’s case “documented Capone's lavish spending, evidence of a colossal income. The government also submitted proof that Capone was aware of his obligation to pay federal income tax but failed to do so." Click here to keep reading about this fascinating case…

Read More

Vehicle and Mileage Issues – Real-World Best Practices and Maximizing Deductions in a Tax Plan

Every tax professional has at least one client that when asked about business mileage replies, “I don’t know; what did I have last year?” You may have read that last sentence and thought, “most of them.” Self-employed taxpayers generally know they must track their mileage, but it’s seldom done correctly, or at all. Vehicle deductions are an area frequently challenged by the IRS on examination as well as an area the taxpayer is unlikely to prevail without strong, contemporaneous documentation. That said, very few taxpayers keep perfect records, so what are the best practices for mileage deductions in the real world? Keep reading to find out!

Read More

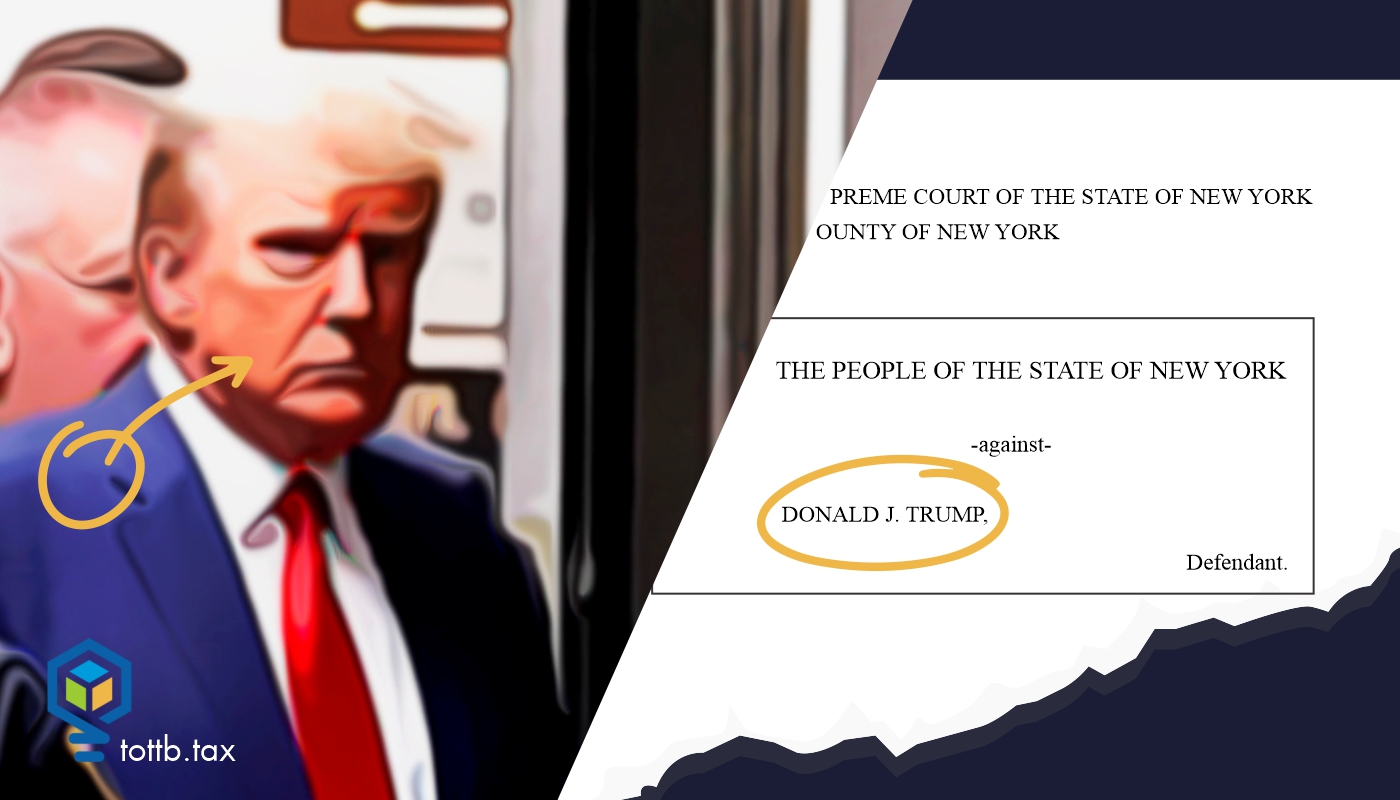

Trump Indictment: An Accountant’s Perspective

IRC § 1031 exchanges have the ability to confer substantial financial benefits to taxpayers. Although taxpayers may use § 1031 to place themselves in a superior economic position, taxpayers may not exploit this section in an abusive manner. Taxpayers can use exchanges to give themselves different types of benefits, but one of the primary benefits is the deferral of federal income tax. When conducted correctly, 1031 exchanges are regarded as a form of legitimate tax avoidance. One of the main issues involved with these transactions is determining the boundaries between abusive tax avoidance and non-abusive tax avoidance. In the context of “related party exchanges” – i.e. those transactions which involve subsection 1031(f) – this issue shows up in a relatively complex fashion, because the related party rules are not well understood by most practitioners. Furthermore, determining abusive tax avoidance with related party exchanges is difficult because of the scarcity of case law. Based on the case law which we have, and on the other authoritative references, we can put together a reasonable overview of the risks of related party exchanges. This overview should prove useful when providing expert counsel to taxpayers seeking to conduct this type of transaction. For direct exchanges, the 2-year ownership rule found in 1031(f)(1)(C) should be used as the dominant source of guidance. For “indirect exchanges,” taxpayers must be aware of the higher levels of risk involved, as there is a greater possibility of abusive tax avoidance. To read more click here!

Read More

Divorce and Taxes

“Timalyn, Alyssa and I filed for divorce, and we will finalize everything before Thanksgiving. Does this change things for our taxes?” “No! Can we wait until January 1?” were my initial thoughts. But then I realized that if this news blindsided me, the seemingly happy couple was probably also scrambling for answers. They were looking to me to be calm during an upcoming storm. To give you some context, I had helped this family lower their back taxes by $16,000 and get a payment plan that worked well with their cash flow. Then, by implementing a few strategies they had just saved an extra $20,000 on their last tax return. We were planning on saving them even more money in upcoming years. Then, that is when it happened. Divorce. I never saw this happening, so I never prepared for it. But if it happened to me, it will happen to you. Clients divorce. Some of the things we are going over today may seem obvious to you. But remember what is obvious to us as tax experts is not obvious to our clients, especially if they are going through a life-changing event such as divorce. Here are four things you need to inform your client about when it comes to their divorce and taxes...

Read More

Worrisome Messages Subtly Delivered Via Recent Tax Developments

Tax professionals are inundated with tax developments from all branches of the government and from all levels of government on a daily basis. Our technical tax knowledge expands weekly. Given the immensity of tax law changes in P.L. 119-21 (July 4, 2025), informally named the One Big Beautiful Bill Act (OBBBA), and the guidance we’ll continue to get over the next few years along with non-OBBBA updates, we might run out of time and bandwidth to step back and ask what additional relevance this guidance, as well as various reports issued by the government every day, mean for the well-being of our tax system. This article unpacks select tax law changes and government documents to offer four subtle messages within them. Generally, the messages don’t bode well for an effective tax and revenue system. The article ends with some suggestions on what can help improve our tax system.

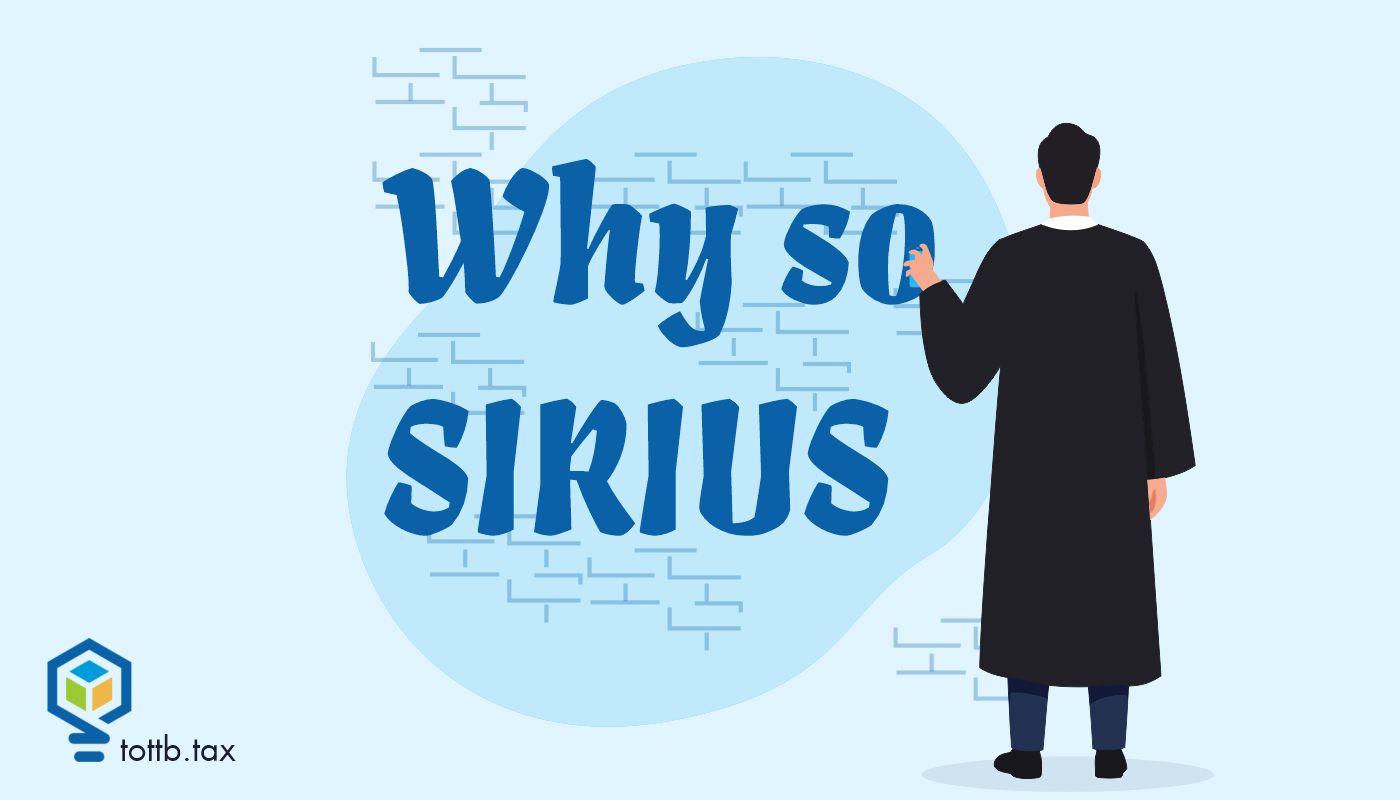

Sirius Solutions and the S Corp or Partnership Choice

The Fifth Circuit Court of Appeals opinion in Sirius Solutions L.L.L.P. v. Commissioner may change our views of entity choice. If the decision holds up, partnerships will be able to effectively make the portion of limited partner income subject to self-employment tax whatever they want, including zero. This contrasts with the IRS position upheld by the Tax Court in Soroban Capital that treated all of the income of limited partners who were active in the business as self-employment income.

Niche Down to Scale Up: How Specialization Drives Visibility and Profitability

For many accountants, narrowing our focus can feel risky. We are trained to serve anyone who needs help and provide stability in any financial situation. Choosing a niche often raises concerns: Will we turn away good clients? Will we limit opportunities or reduce business stability? These are common doubts many of us have faced in our careers.