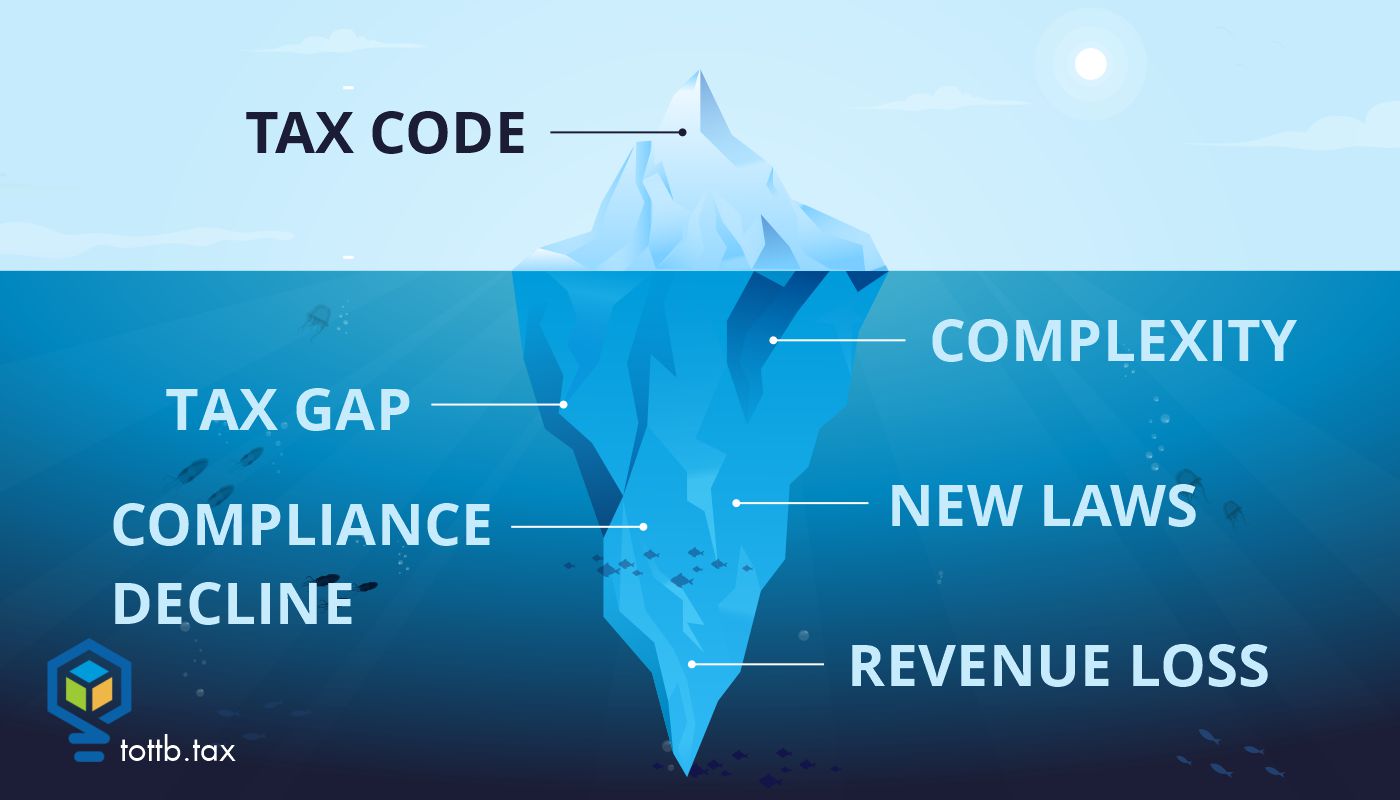

Worrisome Messages Subtly Delivered Via Recent Tax Developments

Tax professionals are inundated with tax developments from all branches of the government and from all levels of government on a daily basis. Our technical tax knowledge expands weekly. Given the immensity of tax law changes in P.L. 119-21 (July 4, 2025), informally named the One Big Beautiful Bill Act (OBBBA), and the guidance we’ll continue to get over the next few years along with non-OBBBA updates, we might run out of time and bandwidth to step back and ask what additional relevance this guidance, as well as various reports issued by the government every day, mean for the well-being of our tax system. This article unpacks select tax law changes and government documents to offer four subtle messages within them. Generally, the messages don’t bode well for an effective tax and revenue system. The article ends with some suggestions on what can help improve our tax system.

READ MORETalking Taxes and Money With New Graduates

Clients who recently graduated college brim with enthusiasm for adult life. If they’re like most other adults, they’re less enthusiastic about tax strategies and probably don’t know much about grown ups’ taxes. Some might not even know filing deadlines and may never have filed a 1040. Withholding, deductions and dependency, saving for retirement and lowering taxable income: It’s always difficult to realize all that others don’t know about taxes, and here’s how to continue these young clients’ education.

Read More

X (Twitter) Strategies for Accountants: Establishing Thought Leadership and Engaging with the Community

Professionals across various fields use X (Twitter) as an essential tool to establish thought leadership, engage with their communities, and grow their influence. For accountants, X offers a unique opportunity to share industry insights, participate in relevant conversations, connect with influencers, and demonstrate expertise. Let's explore how you, the accountant, can leverage X to your advantage, offering practical strategies and real-world examples.

Read More

Editor’s Pick: Tax Planner Faces Malpractice Claims Over Decades-Old Tax Advice—What Went Wrong?

In a case that every tax professional should take note of, the prominent law firm Sidley Austin LLP finds itself defending against claims that it provided faulty tax advice over two decades ago, leading to massive IRS liabilities for a family. The plaintiffs, the Cáceres family, are seeking to recover $7 million after settling with the IRS, claiming Sidley's advice on a complex asset liquidation set them up for disaster. The kicker? The lawsuit was filed over 25 years after the advice was given. So, how are the plaintiffs still able to pursue the case? It all boils down to a claim of fraud—and how that could toll the statute of limitations.

Read More

2024 Winter Education Series Event

Summer may have ended but the education never does here at Think Outside the Tax Box! Join us this winter for our brand-new series of live webinar events spotlighting an intriguing mix of topics all focused on improving you, your business, and your ability to better serve your clients! All of these live events are included FREE with your Basic or Professional subscription and include Continue Education Credits for those who qualify! Winter time is a great time to be part of the Think Outside the Tax Box community! Here are the details of what we have in store for you…

Read More

Navigating IRS Penalty Relief and Forgiveness

Yes, the IRS does forgive some tax penalties. The IRS refers to this forgiveness as penalty abatement. Abatement is the act or process of reducing or removing something. In this case it is removing or reducing a penalty. But penalty forgiveness is not a blanket offer that everyone qualifies for the way the radio ads make it seem. There is a process that the IRS has for requesting and granting abatement. It is up to the taxpayer to prove that they qualify for abatement. That’s where you come in.

Read More

From The Government And Not There To Help You

The story of James J. Maggard has some interesting and possibly valuable lessons. The one that strikes me as particularly important is that it makes it crystal clear that disproportionate distributions contrary to a corporation’s governing documents will not blow its S election. That does not mean that disproportionate distributions are just fine and that you don’t need to address them. There is a practical lesson about being careful who you take on as fellow shareholders. And there is another slightly odd lesson, that almost makes me want to create a new law of tax planning: Don’t deliberately involve the IRS in your business disputes. Their job is not to help you.

Read More

Tax Policy and Reform Considerations for the Next President and 119th Congress

Something we never have a shortage of are proposals to change our tax systems. When it’s election time, we hear even more proposals, as well as how various parts of our tax system are flawed, usually due to actions or inactions of the opposing party. We also hear lots of incomplete statements, promises of tax changes too costly to be enacted, and ideas that will be replaced by the time the winner gets down to crafting a real set of tax and budget proposals. This article describes some of the tax proposals of the two presidential candidates along with suggestions on how we should analyze them against principles supporting effective tax systems, with highlights of some important facts seemingly missing from current tax discussions. These proposals are also relevant to members of Congress as to whether they support any of them and how they align with tax changes that the member would like to see enacted.

Read More

TAX COURT ROUNDUP – October 2024

Much of what happens in Tax Court is run-of-the-mill. Once the tax general practitioner learns the jurisdictional limits and procedural moguls, s/he can advise clients whether to spend the sixty bucks and the certified mail fees when TAS, Examination or Appeals can't deliver an acceptable result. Following the Court's orders and opinions for a while should do that. I try to present the less-than-usual, below-radar points for generalists and specialists.

Read More

Worrisome Messages Subtly Delivered Via Recent Tax Developments

Tax professionals are inundated with tax developments from all branches of the government and from all levels of government on a daily basis. Our technical tax knowledge expands weekly. Given the immensity of tax law changes in P.L. 119-21 (July 4, 2025), informally named the One Big Beautiful Bill Act (OBBBA), and the guidance we’ll continue to get over the next few years along with non-OBBBA updates, we might run out of time and bandwidth to step back and ask what additional relevance this guidance, as well as various reports issued by the government every day, mean for the well-being of our tax system. This article unpacks select tax law changes and government documents to offer four subtle messages within them. Generally, the messages don’t bode well for an effective tax and revenue system. The article ends with some suggestions on what can help improve our tax system.

Sirius Solutions and the S Corp or Partnership Choice

The Fifth Circuit Court of Appeals opinion in Sirius Solutions L.L.L.P. v. Commissioner may change our views of entity choice. If the decision holds up, partnerships will be able to effectively make the portion of limited partner income subject to self-employment tax whatever they want, including zero. This contrasts with the IRS position upheld by the Tax Court in Soroban Capital that treated all of the income of limited partners who were active in the business as self-employment income.

Niche Down to Scale Up: How Specialization Drives Visibility and Profitability

For many accountants, narrowing our focus can feel risky. We are trained to serve anyone who needs help and provide stability in any financial situation. Choosing a niche often raises concerns: Will we turn away good clients? Will we limit opportunities or reduce business stability? These are common doubts many of us have faced in our careers.