A case currently before the Supreme Court, Charles Moore, G. Moore et ux. v. United States , has the court looking at some of the fundamentals of the Constitution’s treatment of taxation. Advocates of various views are hoping for an earthshaking result. Also, many “tax protester” arguments base themselves on misreading of Supreme Court decisions from around the time of the 16th Amendment. Knowing a fuller version of what surrounds the snippets they feed you probably won’t help you bring them around if they have drunk deep of the tax protester Kool-Aid, but it will help you maintain your own sanity. Let’s start with what the Moore case is about.

Worrisome Messages Subtly Delivered Via Recent Tax Developments

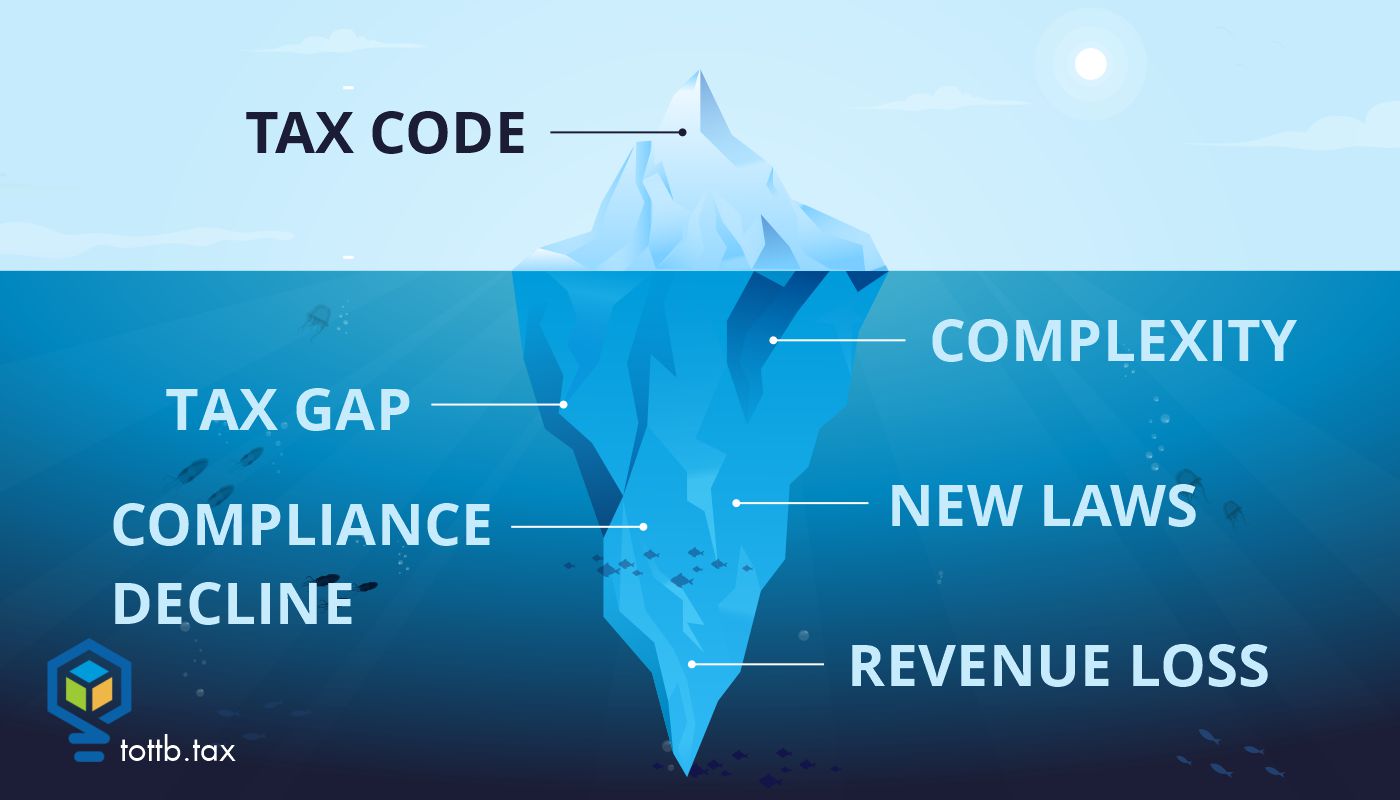

Tax professionals are inundated with tax developments from all branches of the government and from all levels of government on a daily basis. Our technical tax knowledge expands weekly. Given the immensity of tax law changes in P.L. 119-21 (July 4, 2025), informally named the One Big Beautiful Bill Act (OBBBA), and the guidance we’ll continue to get over the next few years along with non-OBBBA updates, we might run out of time and bandwidth to step back and ask what additional relevance this guidance, as well as various reports issued by the government every day, mean for the well-being of our tax system. This article unpacks select tax law changes and government documents to offer four subtle messages within them. Generally, the messages don’t bode well for an effective tax and revenue system. The article ends with some suggestions on what can help improve our tax system.