The inherent optimism of entrepreneurs makes thinking about things that mitigate the effect of failure not that unpleasant. In a career in accounting, you are likely to see many deals that don’t work out, so it’s best to remember anything that will lessen the pain. Section 1244 is such a provision. Section 1244 allows what would otherwise be a capital loss to be treated as ordinary. Its significance has been somewhat diminished, but every little bit helps.

Worrisome Messages Subtly Delivered Via Recent Tax Developments

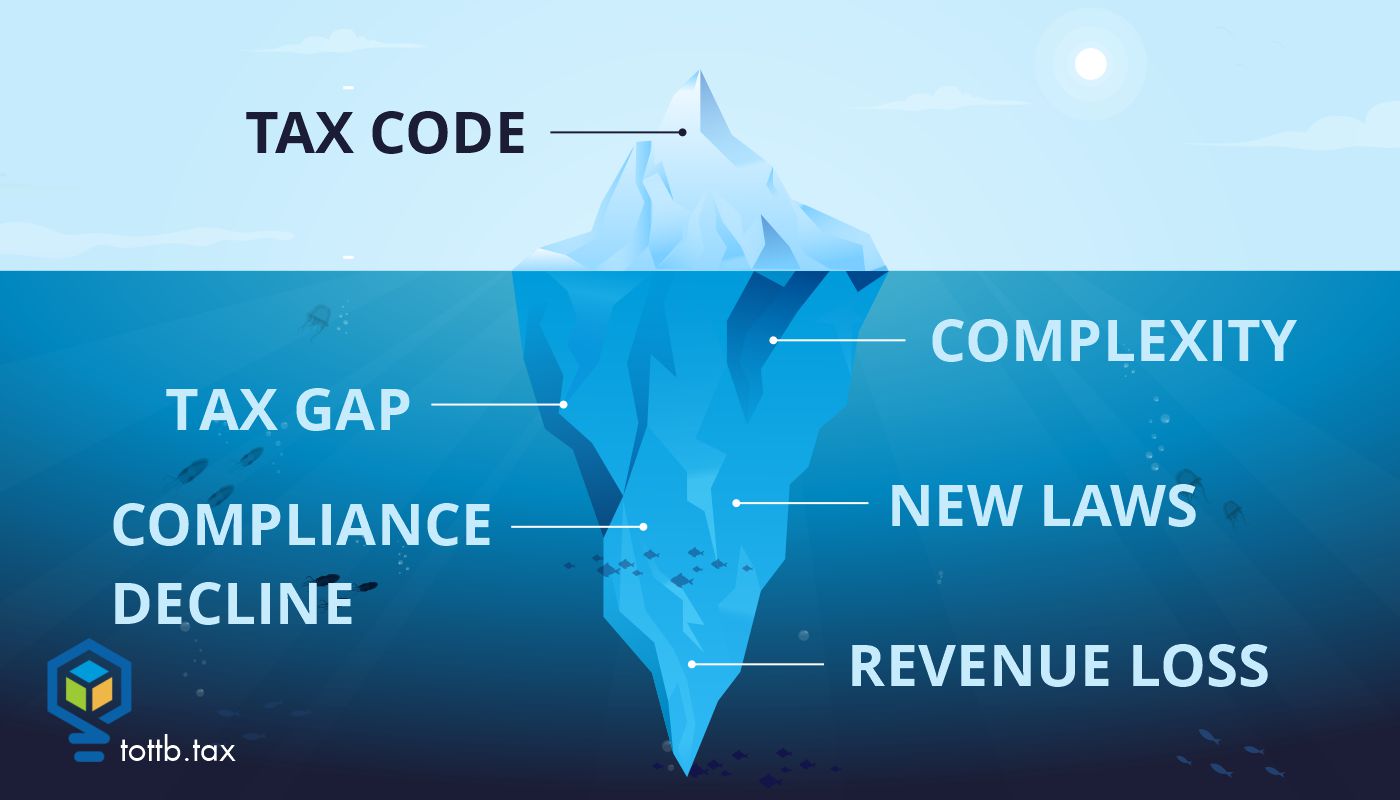

Tax professionals are inundated with tax developments from all branches of the government and from all levels of government on a daily basis. Our technical tax knowledge expands weekly. Given the immensity of tax law changes in P.L. 119-21 (July 4, 2025), informally named the One Big Beautiful Bill Act (OBBBA), and the guidance we’ll continue to get over the next few years along with non-OBBBA updates, we might run out of time and bandwidth to step back and ask what additional relevance this guidance, as well as various reports issued by the government every day, mean for the well-being of our tax system. This article unpacks select tax law changes and government documents to offer four subtle messages within them. Generally, the messages don’t bode well for an effective tax and revenue system. The article ends with some suggestions on what can help improve our tax system.