On the website for Axium Wealth, Charles Dombek tells us that: “Most CPAs are historians that tell their clients how much they make, how much they owe, when and where to file their taxes, and oftentimes how to write large checks at the last minute when you least expect.” When it comes to Axium, though: “We help clients recover dollars they unnecessarily pay in State and Federal income taxes.” Axium also helps clients diversify capital into off-market passive real estate and alternative investments. Before Axium, there was The Optimal-Financial Group LLC. Of course many of the readers of Think Outside The Tax Box are CPAs, or EAs or others who both help their clients be compliant and advise on ways to minimize their liability. When I was practicing I would call the things I might suggest my “bag of tricks.”

Worrisome Messages Subtly Delivered Via Recent Tax Developments

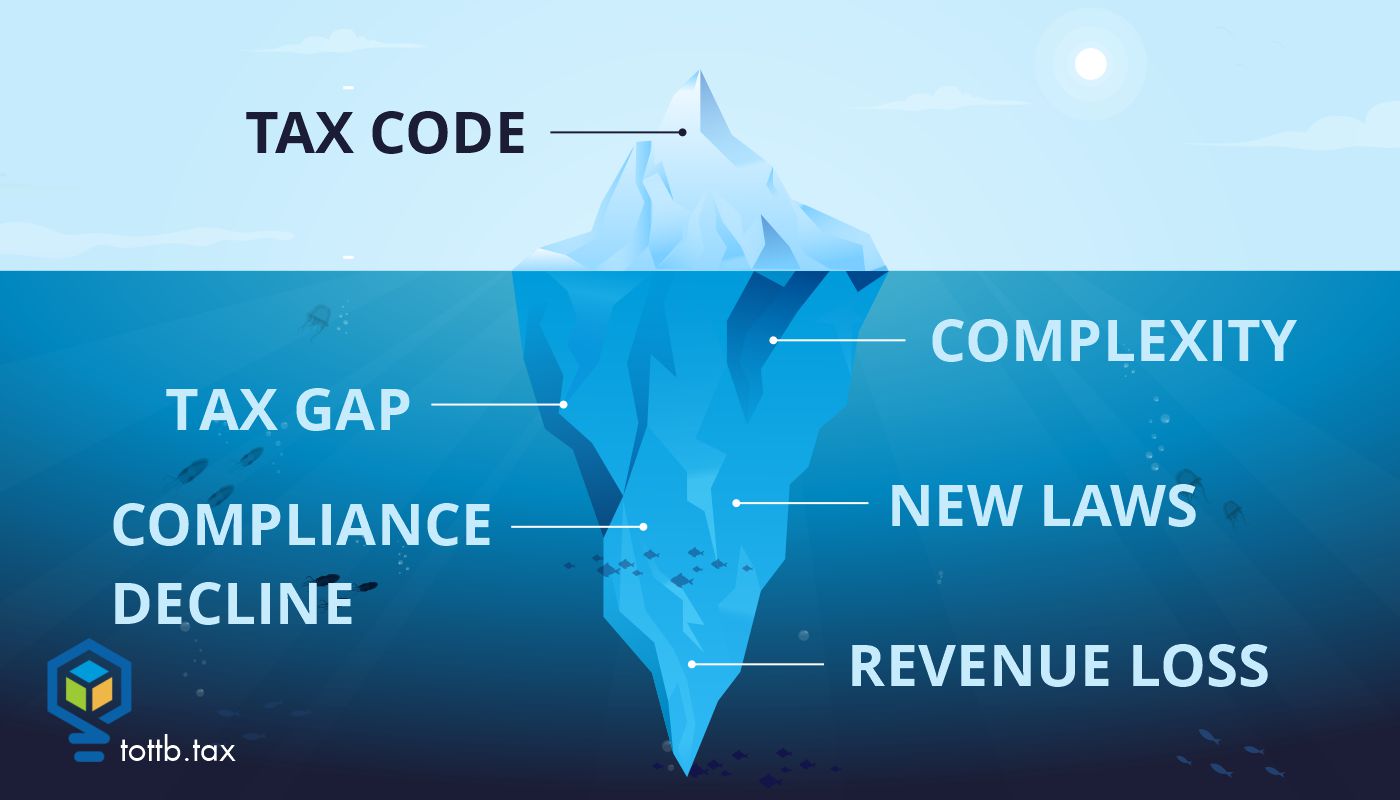

Tax professionals are inundated with tax developments from all branches of the government and from all levels of government on a daily basis. Our technical tax knowledge expands weekly. Given the immensity of tax law changes in P.L. 119-21 (July 4, 2025), informally named the One Big Beautiful Bill Act (OBBBA), and the guidance we’ll continue to get over the next few years along with non-OBBBA updates, we might run out of time and bandwidth to step back and ask what additional relevance this guidance, as well as various reports issued by the government every day, mean for the well-being of our tax system. This article unpacks select tax law changes and government documents to offer four subtle messages within them. Generally, the messages don’t bode well for an effective tax and revenue system. The article ends with some suggestions on what can help improve our tax system.