Ever thought of using a recreational vehicle like a boat to lower your taxes? Yes, it’s possible using the right strategies, and there’s no time like the present to make that happen.

Even more than pre-pandemic taxpayers may be considering buying their own island. Those for whom buying an actual island is beyond the budget may be considering buying a boat or an RV for use as a residence, an office, or both.

Whatever the type of use, there are tax strategies available for boat owners if they meet the requirements. As with any tax strategy it is important to have a full understanding of the requirements to ensure the deduction is legal and to ensure the taxpayer can substantiate the deduction should the tax authorities examine the return.

This is the first of two articles discussing the tax strategies available to boat owners. Part 1 focuses on using a boat as a residence, but if that doesn’t meet your needs, stay tuned because Part 2 will cover boats for business use (including as a home office). Why not consider both options and see how your tax savings can help fund your floating condo? Keep reading to learn more.

Worrisome Messages Subtly Delivered Via Recent Tax Developments

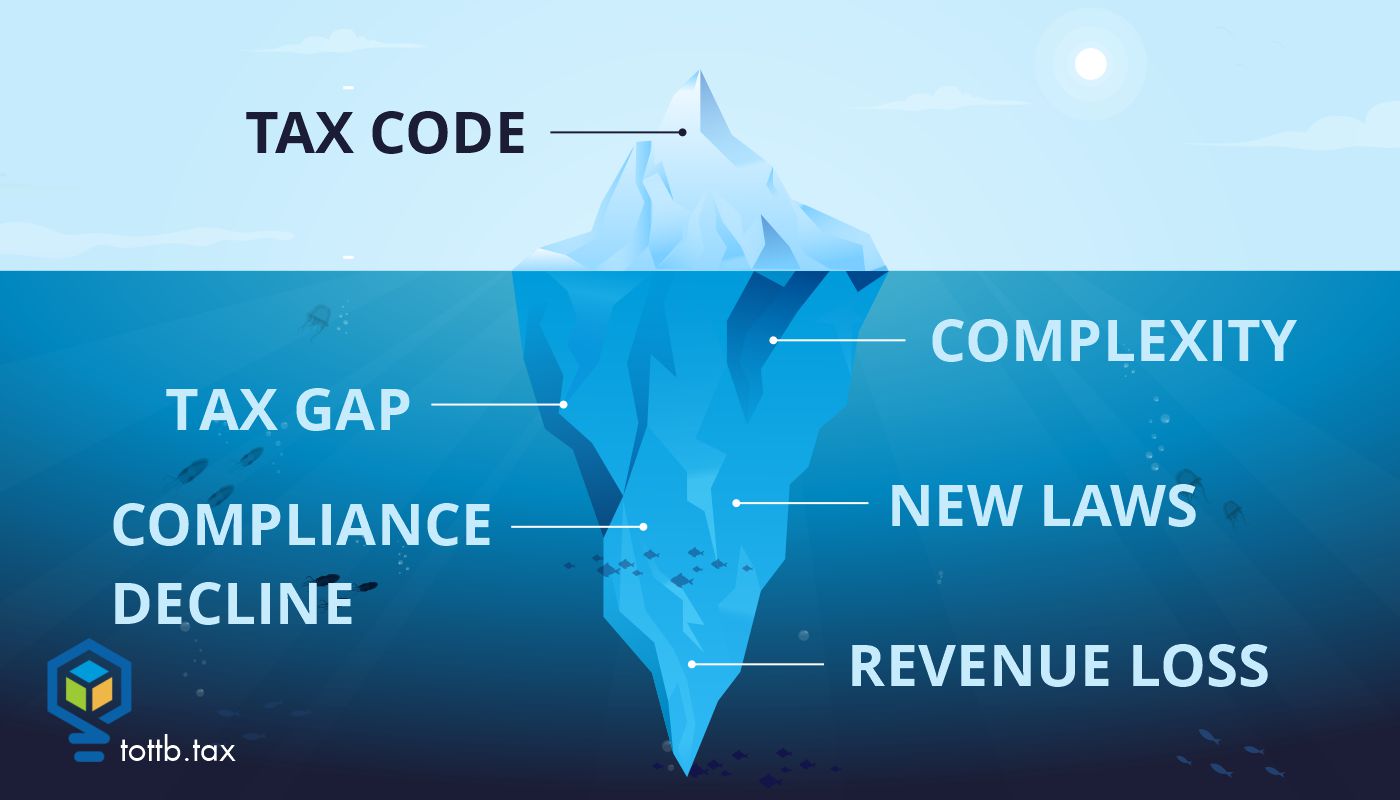

Tax professionals are inundated with tax developments from all branches of the government and from all levels of government on a daily basis. Our technical tax knowledge expands weekly. Given the immensity of tax law changes in P.L. 119-21 (July 4, 2025), informally named the One Big Beautiful Bill Act (OBBBA), and the guidance we’ll continue to get over the next few years along with non-OBBBA updates, we might run out of time and bandwidth to step back and ask what additional relevance this guidance, as well as various reports issued by the government every day, mean for the well-being of our tax system. This article unpacks select tax law changes and government documents to offer four subtle messages within them. Generally, the messages don’t bode well for an effective tax and revenue system. The article ends with some suggestions on what can help improve our tax system.