A Court Just Bought Your Clients More Time on Clean Energy Tax Credits Here’s How to Use It

A federal district court just struck down an IRS rule that had been closing the door on a pretty compelling tax savings opportunity available to your clients today, the Section 48E Clean Electricity Investment Tax Credit. The ruling, handed down on June 6, 2026, reinstated a key pathway that allows investors to lock in credit eligibility for large-scale wind and solar projects a pathway the IRS had tried to eliminate just last year. The window is not wide open. July 4, 2026 is still the critical deadline, and the government will almost certainly appeal. But for advisors who act quickly, this ruling creates a genuine, time-sensitive planning opportunity. Here is what you need to understand, and what you should be doing right now.

READ MORELand Conservation Easements: Tax Avoidance or Evasion?

Question: I was going to look into a conservation easement (CE) for a client and noticed the IRS has focused heavily on compliance efforts for abusive syndicated transactions. Are there any legitimate conservation easement transactions, or is it best to stay away from this strategy until things calm down? Answer: Sounds too good to be true, right? A $500,000 charitable tax deduction for a $100,000 land purchase in December. In your search for information, you may be scared off by the court cases and Department of Justice investigations of the promoters of syndication easements. Syndication deals are partnerships that own land ideal for conservation and allow groups of investors to pool their money in the business, which typically will also include other activities beyond just the land ownership. These deals have come under heavy scrutiny in the past few years as CEs became a listed transaction and more cases have wound their way through the court system. The IRS even announced a settlement program for syndicated conservation easements in mid-2020. Click here to read the full answer.

Read More

Deducting Business Meals and Entertainment: The good, the bad, the very recently changed

“Say dog.” My dad once told me that a friend paid for his lunch and said, “Say dog, then I can write this off.” She bred show dogs. File that under “nope.” That is not how the meals and entertainment (M&E) deduction works. Not even before the Tax Cuts and Jobs Act (TCJA) changed the rules. The deduction for M&E is a favorite of many of our clients and rightfully so. Nevertheless, it can be a fraught area if taxpayers and their advisors don’t have a comprehensive understanding of how the rules for deducting expenses apply across the many different scenarios in which our clients are likely to apply them. The IRS issued the final regulations for deducting M&E expenses under Internal Revenue Code (IRC) § 274 on October 9, 2020. It made some additional, short-term adjustments when the Consolidated Appropriations Act (CAA) became law on December 27, 2020. Here is an overview of the new regulations, how to use them to your clients’ benefit, and how to avoid the most common pitfalls.

Read More

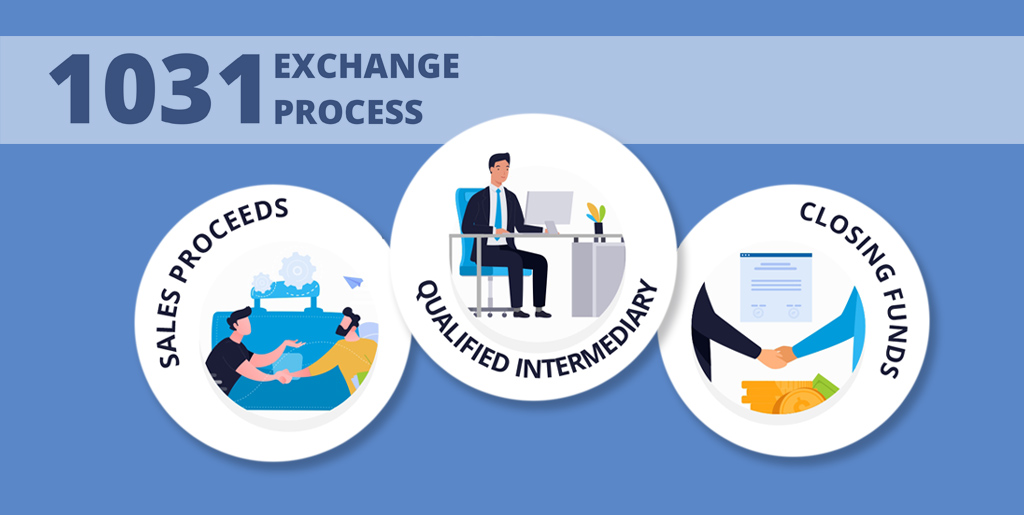

How to Turn a 1031 Real Estate Capital Gain Into a Passive Investment

You may be familiar with the concept of a 1031 exchange as a way to defer gain on the sale of rental or investment real estate. But what happens when you want to completely exit the real estate game? A 1031 Exchange may not be the best option for you. There are a few drawbacks associated with a 1031 exchange, including the limited time frame you must acquire the replacement property, and that you must continue to invest in real estate. If you’re looking to continue deferring current or previously exchanged gains, a Delaware Statutory Trust (DST) may provide a solution to these issues. But investing in a DST property or properties is like any investment. It comes with its own risks and rewards. Read on to find out more.

Read More

Hire Your Kids and Save Money on Your Taxes

Whether you’re preparing to have kids in the future or already have kids, there are tax strategies available (but often overlooked) that you should take advantage of. These are proven ways to save you money on your tax return. How do I know? Well, I use them myself. Bringing children into this world is a great joy and brings immense satisfaction. It’s important to remember, though, having children is a significant responsibility you should take seriously. From a very early age, you need to begin planning for your financial future to ensure you care for your children. There are 10+ unique ways the wealthy families in this country use their families to “qualify” for deductions that often go unused by the middle class. They go unused, not because the middle class can’t qualify; it’s that they don’t make the time to take proactive steps to prepare themselves. Here are just a few of the things you should know as you begin tax planning for your family.

Read More

How To Report Officer’s Compensation For A Late S Election

Question: If I am making a late S election for a client, how do I handle the fact that the officer received no officer’s compensation throughout the year? One of the biggest areas of audit for an S corporation return Form 1120S is officer’s compensation. The IRS collects and examines data from all returns filed and develops a computerized standard of insufficient compensation. Since this area can result in deficiencies for payroll taxes (Social Security and Medicare) for every dollar of distribution reclassified to wage, tax advisors would be wise to avoid risk factors that might raise the risk of audit on officer’s compensation. By avoiding what resembles unreasonably low compensation, we can help business owners by limiting the number of Forms 1120S without officer’s compensation. However, when making a late S election, what is the rule when officer’s truly have taken no compensation? You might be surprised to learn it isn’t filing a Form 1099. Read on to find out how to reduce the risk of audit, while accurately reporting your first Form 1120S.

Read MoreDefer and Eliminate Capital Gains With Opportunity Zones

The Tax Cuts & Jobs Act of 2017 (TCJA) created Opportunity Zones (OZ). Taxpayers who invest in Qualified Opportunity Zones can reduce capital gains tax and pay zero tax on the investment’s future appreciation. For this reason, Opportunity Zones have a significant edge over traditional capital gain deferral strategies like the 1031 Exchange. With more than 8,500 economic zones throughout the United States, investors and business owners have plenty of choices. Additionally, the investment gives them a chance to do some good in an economically depressed area, make some tax-free money, and achieve some permanent capital gain savings even after you’ve already sold your asset. What’s not to love? There are a number of intricate rules concerning OZ investment tax breaks so if you want to begin or expand your business or real estate holdings using these tax breaks, read on to learn more.

Read More

When a 1031 Exchange May Not Actually Save On Tax

The 1031 Like-Kind Exchange (LKE) provides a great potential benefit to taxpayers who want to sell rental properties to purchase others in the United States. IRC § 1031 allows you to defer a taxable gain that would normally be taxed at the time of sale of a rental property. However, there are situations when a 1031 exchange may not be the best option for the taxpayer, and it could potentially dilute the tax savings when compared to a traditional sale or other gain minimization strategies. To take advantage of the tax deferral benefits of a 1031 exchange, you’ll need to follow a specific set of guidelines. Here, we will dive into the circumstances that you should review to determine if a 1031 exchange will be the best option in mitigating the taxes you owe.

Read More

How to Do a Backdoor Roth IRA (Safely) and Avoid the IRA Aggregation Rule and Step Transaction Doctrine

The basic concept of the “backdoor Roth IRA contribution” is relatively straightforward. Contributing directly to a Roth IRA is restricted for higher-income individuals; once a married couple has an AGI in excess of $193,000 (or $131,000 for an individual), the maximum contribution limit to a Roth IRA reduces to zero. However, anyone with earned income can contribute to an IRA, regardless of how high their income is; at worst, higher income levels may limit the deductibility of that IRA contribution (for those who are an active participant in an employer retirement plan), but not the ability to make the IRA contribution. In addition, under the Tax Increase Prevention and Reconciliation Act of 2005 (TIPRA), there have been no income limits on Roth conversions of traditional IRAs since 2010. As a result, anyone who has funds in a traditional IRA, whether originally deductible or not, is eligible to do a Roth conversion. In other words, while income limits remain on Roth contributions, there are no income limits for a Roth conversion.

Read More

A Court Just Bought Your Clients More Time on Clean Energy Tax Credits Here’s How to Use It

A federal district court just struck down an IRS rule that had been closing the door on a pretty compelling tax savings opportunity available to your clients today, the Section 48E Clean Electricity Investment Tax Credit. The ruling, handed down on June 6, 2026, reinstated a key pathway that allows investors to lock in credit eligibility for large-scale wind and solar projects a pathway the IRS had tried to eliminate just last year. The window is not wide open. July 4, 2026 is still the critical deadline, and the government will almost certainly appeal. But for advisors who act quickly, this ruling creates a genuine, time-sensitive planning opportunity. Here is what you need to understand, and what you should be doing right now.

Your Summer Tax Practice Playbook: Three Moves to Make Before Labor Day

Tax Day is finally in the rearview mirror, and if you’re like many practitioners—with the phones quieter, the inbox manageable, and the September extension wave feeling comfortably far away—the temptation right now is to coast. Resist that temptation. Summer is the only stretch of the calendar when both you and your best clients have the bandwidth to think strategically; furthermore, this summer, there is a deadline-driven opportunity. In this article, I’ll walk through three moves every practitioner should be making between now and Labor Day. The first move has a hard statutory deadline of July 10, 2026. The second move is about turning your highest-value client conversations into billable advisory engagements. And third is about tending to the practice itself because a tax practice, like a garden, doesn’t survive without care.

What Every Client Should Know About Partnership Distributions

Perhaps the most misunderstood aspect of partnership taxation relates to distributions. When a partnership distributes cash or property to its partners, the tax consequences can range from completely tax-free to significantly taxable, depending on how the distribution is structured and the partners’ tax basis in their partnership interests. In this article, we’ll explore the rules governing partnership distributions and how they impact partners’ tax situations. More importantly, we’ll look at strategies to structure distributions in the most tax-efficient manner possible – because the goal is not just to understand the rules but to use them advantageously.