Joseph Michael Balint had some really hard luck. He was in prison in Florida from December 17, 2013, through January 6, 2015. Fearful of forfeiting assets, he transferred everything to his wife, Jacqueline, and gave her power of attorney early in his prison term. What he had not planned on was her emptying the retirement accounts and leaving him with the tax tab. His luck turned a bit in Tax Court, as we shall see.

Worrisome Messages Subtly Delivered Via Recent Tax Developments

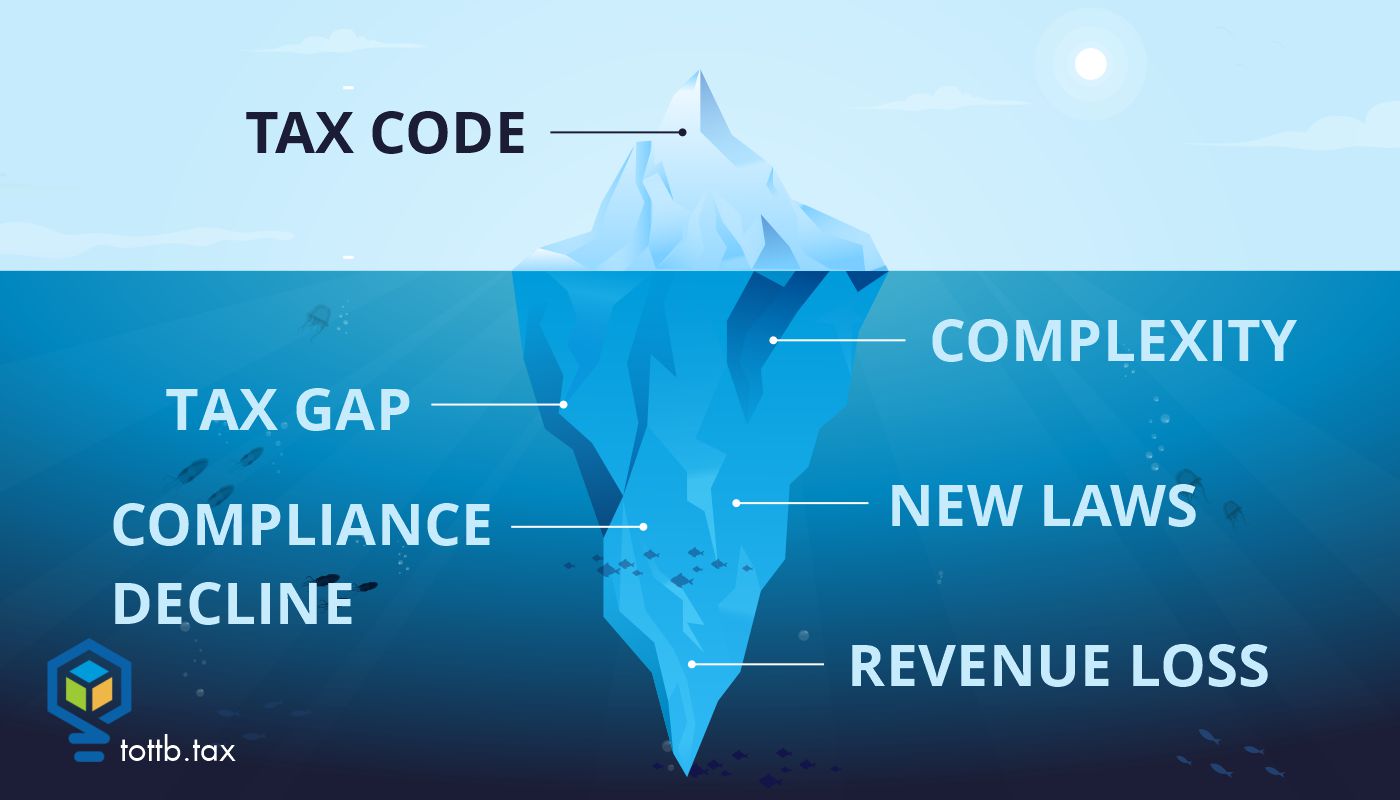

Tax professionals are inundated with tax developments from all branches of the government and from all levels of government on a daily basis. Our technical tax knowledge expands weekly. Given the immensity of tax law changes in P.L. 119-21 (July 4, 2025), informally named the One Big Beautiful Bill Act (OBBBA), and the guidance we’ll continue to get over the next few years along with non-OBBBA updates, we might run out of time and bandwidth to step back and ask what additional relevance this guidance, as well as various reports issued by the government every day, mean for the well-being of our tax system. This article unpacks select tax law changes and government documents to offer four subtle messages within them. Generally, the messages don’t bode well for an effective tax and revenue system. The article ends with some suggestions on what can help improve our tax system.