Office security. It’s for you and your small business clients. Sometimes small business clients who have relatively low-tech operations don’t think they need to think much about office security. That’s just not true. Almost every small business has some level of liability exposure for theft of client information or their own information (banking, credit cards, account passwords, etc.)—even businesses that don’t consider themselves “web based” or “high tech” may have client or company proprietary information they want to keep secure and private. Often business owners focus on cyber security (and with good reason). But a good, comprehensive security plan creates a safety triangle around important information and the property that holds it. The three sides of this triangle are cyber security, physical security, and (at the base of it all) operations security. Keep reading to secure your future!

Small Mistakes With Huge Costs for Your Client’s Tax Returns

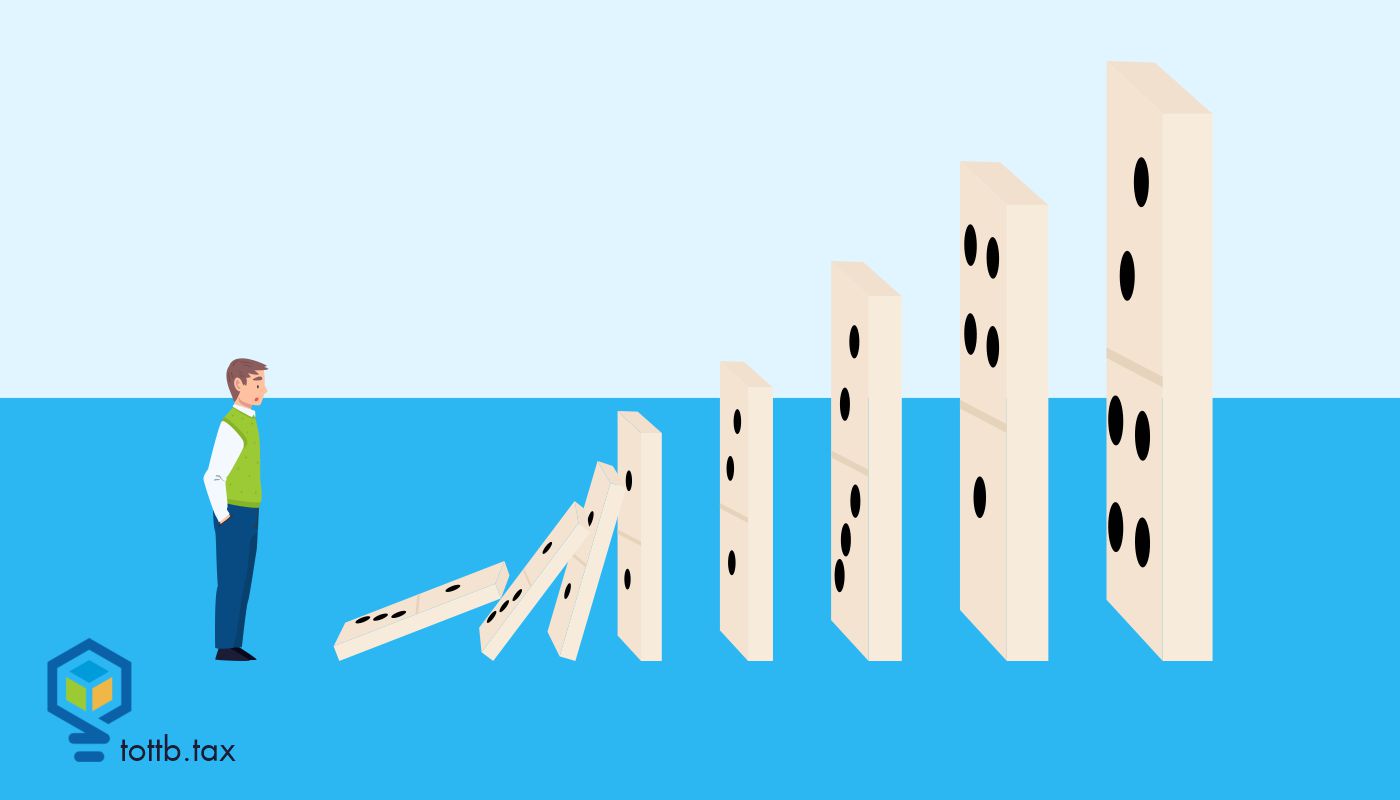

We’ve all been there. A client walks into your office and, somewhere in the conversation, you realize that a seemingly minor oversight, a missed deadline, a form nobody filed, an election nobody mentioned, has spiraled into a five- or six-figure tax problem. In my years of practice, some of the most expensive mistakes I’ve seen weren’t the result of aggressive planning gone wrong. They were small, quiet errors. The kind that happens when a deadline slips, an election isn’t made, or a form gets overlooked entirely. The tax code is unforgiving in these situations, and the IRS has little sympathy for “I didn’t know.” This article walks through some of the most common, and most costly, small mistakes that can devastate your client’s tax situation, along with practical guidance for avoiding them.